With the Fed in a political tug‑of‑war and global inflation fears flaring, currency markets are on high alert. On Aug. 29, rising Aussie prices, shaky Fed signals and a crude crash could spark wild moves in AUD/USD, EUR/USD and USD/CAD. Traders are bracing for a perfect storm of central bank drama and data surprises.

A brewing Fed independence crisis and fresh inflation jitters are setting FX markets on edge. In recent days Fed officials (and even President Trump) have hinted at imminent rate cuts, sending U.S. stocks higher and the dollar tumbling. Meanwhile in Asia a surprise jump in Australian CPI has lifted AUD/USD to multi‑week highs, and crude oil is languishing near two‑month lows around $62 a barrel. This toxic mix of central bank politics, sticky prices and sliding commodities is building into a volatile finish for August. Traders will watch key chart levels and end‑month flows across AUD/USD, EUR/USD and USD/CAD, as technical breakouts loom and economic data (Fed’s favored PCE, German CPI, Canada GDP, etc.) hits the wires.

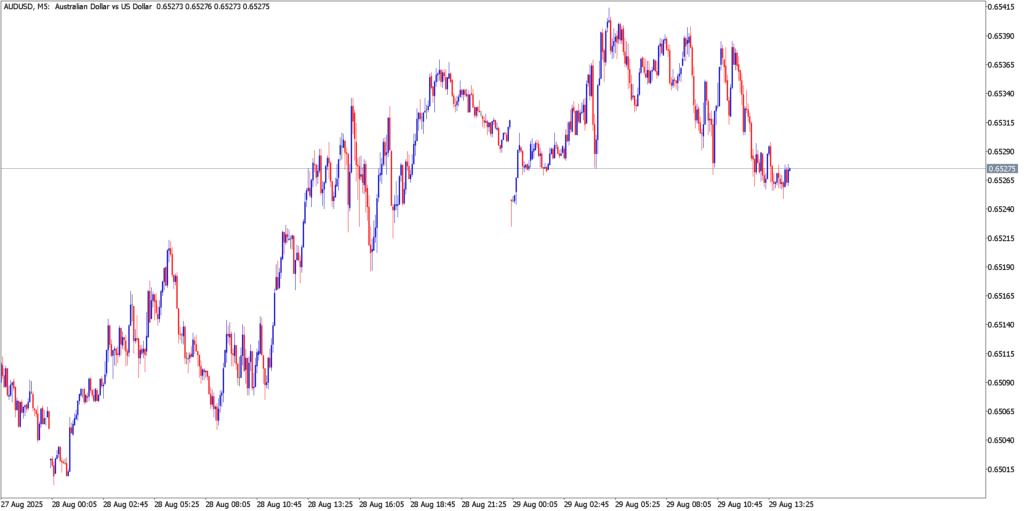

AUD/USD

The Aussie dollar is in a short‑term uptrend. After jumping past 0.6500 on Thursday, AUD/USD tested a two‑week high. Key resistance now sits around 0.6553–0.6567 (Daily R1–R2), with strong support near 0.6516 and 0.6502 (Daily S1–S2) as noted in recent technical tables. Momentum indicators remain bullish (RSI>50, MACD buy signals), suggesting the pair could probe the upper 0.65‑0.66 range if buyers hold above 0.65. A break above 0.6567 would open the door toward 0.6580+; on the downside a fall below ~0.6500 would target the 0.6480s.

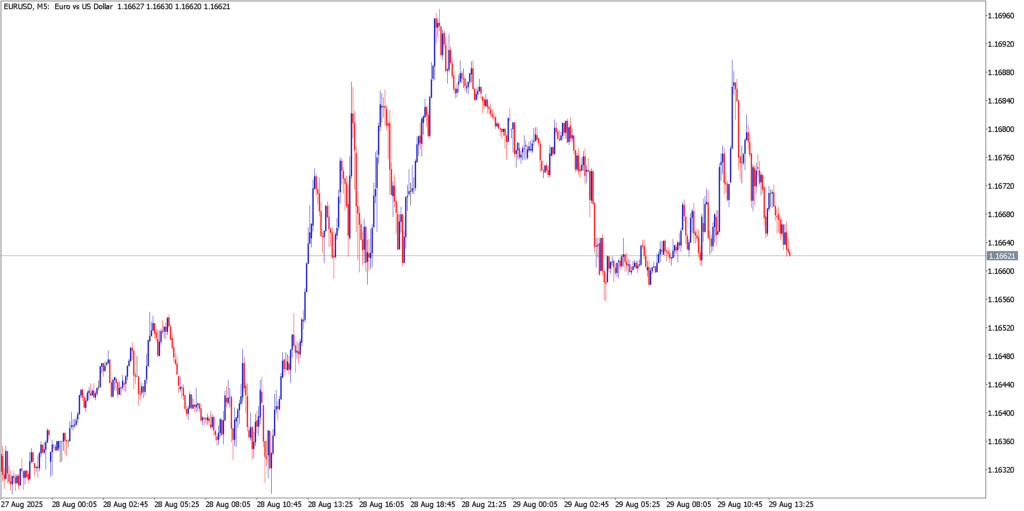

EUR/USD

EUR/USD has been range‑bound around 1.16–1.17. The 50‑day EMA (~1.1600) is acting as immediate support, while resistance clusters near 1.1700–1.1730 (the high‑end of the range). Recent rallies stalled under ~1.1720, and Thursday’s 0.4% gain stalled around 1.1690. A decisive break above 1.17 could target the 1.1800 region (and ultimately 1.20+ per chart targets), while a drop below 1.1650/1.1600 would risk sliding back toward 1.1550. Overall technicals point to consolidation: the 50‑DMA near 1.16 is support, and RSI sits mid‑range. In short, EUR/USD is coiling for its next leg – a breakout or breakdown could be triggered by Friday’s data.

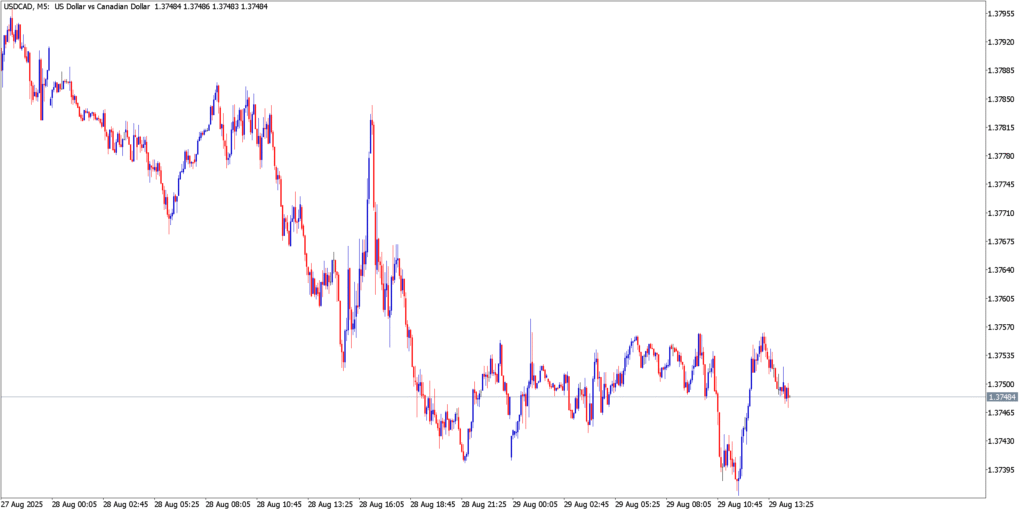

USD/CAD

The Loonie strengthened into Friday, putting USD/CAD under pressure. On Thursday the pair dipped to about 1.3750 – roughly the 50‑day EMA and a prior support zone – before rebounding slightly. Technical support is now ~1.3750, with resistance at 1.3800 and the next barrier around 1.3900. This price action looks like a rounding bottom: if USD/CAD breaks above 1.38/1.39, it could resume a steeper downtrend. Conversely, a firm break below 1.3750 would target 1.3700 and open a further slide. In sum, USD/CAD has a short‑term base at 1.3750; traders will watch closely to see if it holds. (A breach of 1.3750 on strong dollar flows could spark a fast drop.)

Fundamental Analysis

The economic calendar is packed with high-impact releases. The U.S. publishes July’s PCE inflation (Fed’s preferred gauge) and core PCE (expect +0.3% m/m) at 13:30 GMT. At 13:00 GMT Germany’s preliminary Aug CPI (forecast +2.1% YoY) will set the tone for the euro. Canada reports Q2 GDP at 13:30 (annualized ~–0.6%). Other releases include final UoM August sentiment (15:00 GMT) and Japan’s July retail sales. In short, traders will scrutinize U.S. inflation vs. Euro‑zone inflation and Canada’s data to gauge central bank policy.

- U.S. PCE (Jul): Core PCE is expected +0.3% m/m. A stronger-than-expected number would boost the USD (denting EUR/USD) by reducing Fed cut odds. A softer print would reinforce bets on a Fed rate cut this autumn, weighing on the greenback and lifting EUR and AUD.

- German CPI (Aug): Markets look for a slight uptick to +2.1% YoY. If Germany (and Euro‑area) inflation surprises on the upside, it would temper ECB easing expectations and support EUR. If inflation slows instead, it would cement ECB rate-cut bets and pressure the euro.

- Canada GDP (Q2): A forecast contraction (~–0.6% annualized) would underscore Canada’s growth woes. Combined with July CPI at just 1.7% YoY, a weak GDP print would lock in expectations of BoC rate cuts, keeping CAD soft (pushing USD/CAD higher). Conversely, any upside surprise would be hard to find.

- Australia: Note Australia has no major releases on Aug 29, but Thursday’s CPI (+) means the RBA can stay cautious. Recent economic trends (tourism rebound, trade shock from tariffs) argue for patience. In practice, firm Aussie inflation and a dovish Fed bias both tip the scales in AUD’s favor in AUD/USD.

- Global risk: Fed Chair Powell’s dovish Jackson Hole talk (Aug 22) has already sent the dollar lower and stocks higher. Risk sentiment remains fragile given geopolitical tensions and month‑end flows. As the XTB calendar notes, tariff‑related distortions may also bump up August PCE inflation slightly, so traders must read the tea leaves carefully.

The US‑Australia outlook is now pivoting on Fed vs RBA cues. A soft U.S. PCE (or hawkish Fed retreat) would likely push AUD/USD above 0.66 as the Aussie holds Friday’s gains. For EUR/USD, the battle between U.S. inflation (Fed) and German/EZ inflation (ECB) will decide direction: weak U.S. PCE could lift EUR/USD from its 1.16 base, whereas a strong German CPI might also prop up the euro and cap downside. Lastly, USD/CAD is largely driven by oil and BoC expectations. Canada’s weak CPI and GDP (and oil at ~$62) mean the Loonie is under pressure. Unless oil bounces, USD/CAD is biased higher from 1.3750 toward 1.38–1.39. However, any dramatic U.S. data surprise could reverse flow into CAD briefly.