Thursday’s trading (Nov 6, 2025) delivered high drama across major currencies. The mighty U.S. dollar finally stumbled, sending the euro soaring back above $1.15, the pound clinging to the critical $1.30 threshold, and the Aussie dollar springing past $0.65. Traders were caught off guard by a potent mix of technical breakouts and fundamental bombshells, from a nail-biting Bank of England showdown to surprising signals in U.S.–China trade. By day’s end, the stage was set with the dollar on its back foot and once-battered counterparts seizing the spotlight in spectacular fashion.

EUR/USD

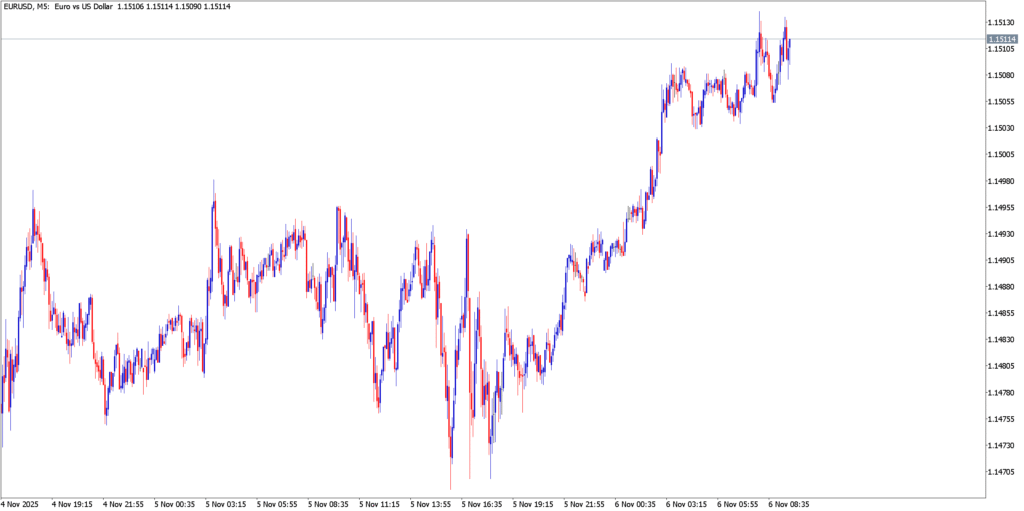

Technical Analysis

After flirting with multi-month lows, EUR/USD staged a sharp intraday reversal on the 5-minute chart. Just a day after plunging to around 1.1473 (a three-month low), the pair ripped higher, shattering the $1.1500 barrier with authority. Once that psychological resistance gave way, it promptly flipped into support – dips toward $1.1500 were swiftly bought, showing newfound bullish resolve. The M5 chart revealed a series of higher lows and a bullish breakout from early-day consolidation, signaling momentum had decisively shifted upward. Euro buyers drove the surge toward the mid-1.15s, where the rally met resistance near the day’s highs (just above $1.1510). Although the upside momentum eased slightly at that ceiling, EUR/USD comfortably held its gains, trading above its intraday moving averages and keeping the short-term uptrend intact into the close.

Fundamental Analysis

The euro’s ascent had less to do with Eurozone news and everything to do with a softening U.S. dollar. With no major EU data releases on the day, traders took cues from across the Atlantic – and the signals all pointed to a breather for the greenback. Encouraging U.S. labor data mid-week had pushed Treasury yields higher, but paradoxically the dollar couldn’t capitalize. A resurgence in global risk appetite – sparked by a rebound in equities and optimism in trade relations – sapped demand for safe-haven USD. In Washington, a prolonged government shutdown left investors “flying blind” on economic reports, injecting uncertainty that further undermined the dollar’s appeal. Sensing an opening, euro bulls ran with it. The distinctly weaker dollar lifted EUR/USD back above $1.15, erasing its earlier losses. While the ECB’s rate is now roughly half of the BoE’s (after a year of cuts to ~2% vs. BoE’s 4%), policy divergence took a back seat to U.S. developments. In short, fading Fed hawkishness and a return of risk-on sentiment gave the euro a dramatic reprieve, allowing it to rocket off its lows and reclaim a key level in one trading session.

GBP/USD

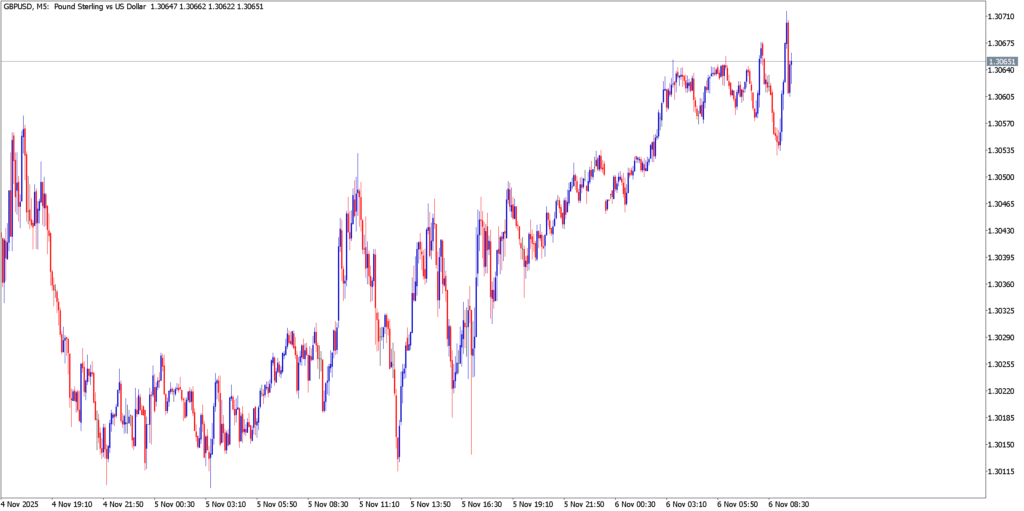

Technical Analysis

GBP/USD spent the day in suspense, trading in a narrow, nervous range as markets braced for the Bank of England’s verdict. On the 5-minute chart, the pair’s recent six-day slide finally stalled, finding an apparent floor just above $1.3000. In the Asian pre-market hours, sterling wilted to a seven-month low at $1.3011, but bears failed to crack the 1.3000 handle – a line in the sand that bulls fiercely defended. This resulted in a double-bottom base around $1.301–1.303 as the session progressed. Every dip toward the low-$1.30s was met with eager buying, while intraday bounces were capped in the mid-$1.30s (around $1.3070). The tight coiling of price action reflected trader trepidation: no one wanted to commit big positions before the BoE. By late session, GBP/USD remained glued near $1.305, its 50-period M5 average flat, illustrating the market’s indecision. The technical picture showed a spring coiled – whichever way the BoE went, an eruption seemed imminent after hours of pound consolidation.

Fundamental Analysis

The Bank of England’s policy meeting was the day’s showstopper, and it delivered pure suspense. Heading into Thursday, sentiment around the pound was grim – sterling had been tumbling, down over 3% in the past month as traders bet the BoE might slash rates. Bets on a cut had surged from virtually nothing a month ago to nearly 30–40% odds of a 25 bp cut on the day. Analysts openly warned of a “knife-edge” decision, and the atmosphere was charged with uncertainty. In the end, Governor Andrew Bailey and team held rates at 4.0%, but it was a close call – reportedly a 5–4 split vote to stand pat, meaning nearly half the MPC wanted an immediate cut. The BoE delivered a dovish hold, signaling that while they didn’t pull the trigger this time, an easing cycle is looming. The rationale was clear: UK inflation, though still 3.8% (G7’s highest), has plateaued, and a big fiscal tightening is coming (Finance Minister Rachel Reeves’ budget on Nov 26 is expected to hike taxes, potentially cooling the economy). Bailey’s message in the press conference was cautious – with inflation pressures easing and clouds on the economic horizon, rate cuts are likely only a matter of time. For the pound, the lack of an actual cut provided brief relief; GBP/USD spiked slightly higher on the no-change announcement. But any celebration was muted by the BoE’s overtly dovish tone. Realizing that rate relief is merely delayed, not denied, traders kept sterling’s gains in check. By the end of the day, GBP/USD was essentially flat (down 0.01%), hovering just above $1.305 – the pound exhaled a sigh of relief, but the clouds of future rate cuts kept enthusiasm in check.

AUD/USD

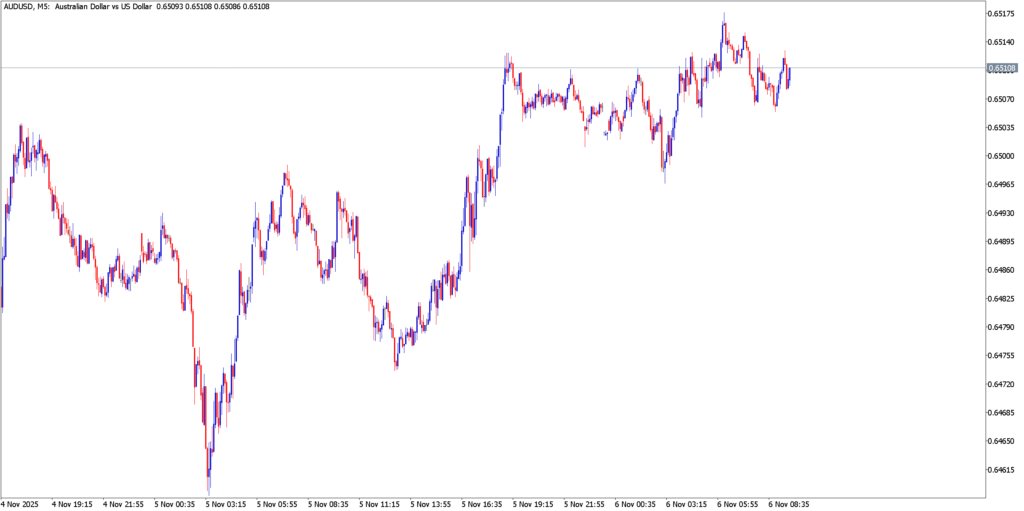

Technical Analysis

AUD/USD charged higher on Thursday, riding a wave of risk-fueled buying. The 5-minute chart shows the Aussie forming a steady intraday uptrend, a stark reversal from the prior day’s pullback. In early trading, the pair bounced off a three-week low near $0.6470–0.6480, establishing that zone as solid support. From there, it was off to the races: the Aussie marched upward in a series of higher highs and higher lows, slicing through the $0.6500 level and continuing to grind north. By midday, AUD/USD was trading above $0.6520, the bulls having erased the week’s earlier losses. The momentum did slow as the pair approached the mid-$0.65s – an area that attracted some profit-taking – but notably, no significant pullback ensued. Every minor dip was met with fresh bids, and the pair remained above its short-term moving averages throughout the climb. This persistent bid tone kept AUD/USD near its session highs into the close, reflecting a confident technical breakout from the week’s doldrums.

Fundamental Analysis

The Australian dollar’s rally was underpinned by one major theme: risk-on fervor. A sharp rebound in global stock markets and commodities bolstered risk-sensitive currencies, and the Aussie – often a proxy for market sentiment – thrived in this environment. Traders largely shrugged off the usual dollar-supportive factors (like rising U.S. yields) and instead latched onto positive headlines from China and the U.S.. Notably, China’s first purchase of U.S. wheat in over a year made waves. This gesture of goodwill in trade was interpreted as a green light for commodity currencies: it signaled improving trade relations, which lifted Australia’s outlook as a commodity exporter. Domestically, there were no negative surprises to spoil the party. Earlier in the week the RBA had held rates steady at 3.60% (widely expected, with no further cuts likely until 2026), so the policy backdrop remained stable for AUD. With the central bank in wait-and-see mode and Australian data releases scarce, external factors took the driver’s seat. The result was a classic “risk rally”: as market confidence grew, the Aussie’s losses evaporated. By day’s end, AUD/USD’s uptick, while modest in percentage terms, marked a significant reversal of fortune from its earlier lows. The currency that started the day under pressure ended it energized and higher, buoyed by global optimism and a rekindled appetite for risk.

Market Outlook

After this dramatic session, forex traders are on high alert for what comes next. The U.S. dollar’s slip has injected uncertainty into a market that had been trending dollar-positive for months. Upcoming U.S. economic data – especially the nonfarm payrolls report due Friday – could either reinforce the dollar’s decline or give it new life, making it a pivotal focus as the week closes. If the jobs data (or any delayed reports once the government shutdown clears) show unexpected strength, the greenback may find its footing again; conversely, any weakness could accelerate the dollar sell-off that benefited EUR, GBP, and AUD this week. In Europe, the euro will watch for any hints from the ECB or inflation figures that could either validate or undermine its newfound strength. For the pound, attention shifts to post-BoE signals: commentary from MPC members and the tone of the November 26 UK budget will be crucial. Traders know that any sign of economic stress or dovish leanings could revive pound volatility, especially with the BoE seemingly one meeting away from a cut. The Australian dollar will take cues from the trajectory of global risk sentiment – further improvements in U.S.-China relations or continued equity rallies could extend its gains, while any risk-off shock (be it geopolitical flare-ups or disappointing Chinese data) could quickly put the Aussie on the back foot again. Volatility is the name of the game as we move forward. The dramatic moves of November 6 have shown that entrenched trends can turn on a dime. With multiple central banks at inflection points and geopolitical undercurrents (like U.S. trade policy and global conflicts) simmering, the stage is set for more fireworks in the currency markets. Traders will be watching key levels – can EUR/USD sustain its break above 1.1500? Will GBP/USD hold the line at 1.3000 amid looming rate cuts? Can AUD/USD build on its risk-fueled rally? The answers will unfold in the days to come, but one thing is certain: after a day of such high-stakes drama, nobody is taking their eyes off this market. Stay tuned – the next act in this forex saga may be just around the corner.