The forex market kicks off the week of November 17, 2025, with high drama across major currency pairs. The US dollar is flexing its muscles against the Japanese yen – USD/JPY has surged to levels not seen in decades, stoking speculation about potential intervention as Japan’s currency teeters. Meanwhile, GBP/USD remains under pressure, hemmed in by Britain’s economic struggles and waning bullish momentum. In contrast, EUR/USD is showing signs of life, attempting to rally on the back of a softening dollar and relatively stable Eurozone outlook. Traders are navigating a landscape of diverging fundamentals: a yawning US-Japan interest rate gap weakening the yen, UK-specific economic woes weighing on sterling, and the euro finding support as markets eye a narrowing policy gap with the US. Below we break down the technical picture and key drivers for each of these pairs, followed by an outlook for what’s ahead.

USD/JPY

Technical Analysis

USD/JPY exploded higher in recent sessions, piercing above ¥154 to reach its highest levels in over 25 years before a sharp intraday pullback. The 5-minute chart reveals how the pair rocketed to roughly ¥154.4 on a burst of dollar strength, only to recoil back toward the mid-153s as sellers swiftly stepped in. This whipsaw price action indicates heavy resistance in the 154.0–154.5 zone, where profit-taking and possible official intervention talks intensified. Despite the volatility, the short-term uptrend remains largely intact – the pair is still printing higher lows on the M5 timeframe, and dips have been shallow. Support emerged around ¥153.6–¥153.8 during the retracement, suggesting buyers are eager to defend any pullback. Momentum indicators show USD/JPY still on strong footing, but the double-top potential near the recent peak hints at exhaustion. In the very near term, consolidation is setting in just above ¥154.0 as bulls catch their breath. A clear break above ¥154.5 would signal continuation of the bullish trend, whereas a fall below ¥153.5 (near last week’s support) could mark a deeper correction after the steep climb.

Fundamental Analysis

Fundamentally, the yen’s weakness is rooted in a growing policy divergence and economic challenges at home. The Bank of Japan remains ultra-accommodative – it left interest rates near 0% in its late-October meeting – and even as Japanese 10-year bond yields have crept up to multi-year highs, officials in Tokyo show little urgency to tighten policy. In fact, recent remarks from Japan’s leadership signaled resistance to any rapid BOJ rate hikes, reinforcing the view that Japan will stick with low rates to support its fragile economy. This stance has emboldened yen sellers, given the stark contrast with US monetary policy. The Federal Reserve, while pausing further rate increases, is still maintaining a benchmark rate near 5%, keeping US-Japan yield differentials extremely wide. That gap invites carry trades that favor borrowing yen (at near-zero cost) to buy higher-yielding USD assets – a recipe for continued USD/JPY strength. Additionally, Japan’s latest economic data underpins the yen’s vulnerability: third-quarter GDP contracted around 0.5%, and export growth has been dented by global trade frictions (including new U.S. tariffs on Japanese and European goods). This weak growth outlook pressures the BOJ to stay dovish, further undermining the yen. It’s no surprise then that USD/JPY’s rally has been relentless. However, these lofty levels also raise the specter of intervention. Japanese officials have a history of stepping into FX markets when yen depreciation becomes too rapid or destabilizing. With USD/JPY now well beyond the psychological ¥150 line and pushing into mid-150s, markets are on high alert for any verbal warnings or direct market action from Japan’s Ministry of Finance. In summary, the fundamental bias remains upward for USD/JPY as long as the Fed-BOJ policy gulf persists, but the risk of an intervention-induced jolt is growing by the day. Traders should be cautious about potential headline surprises – any hint of policy shift from the BOJ or explicit intervention threats could trigger a swift yen rebound even as the broader uptrend still favors the dollar.

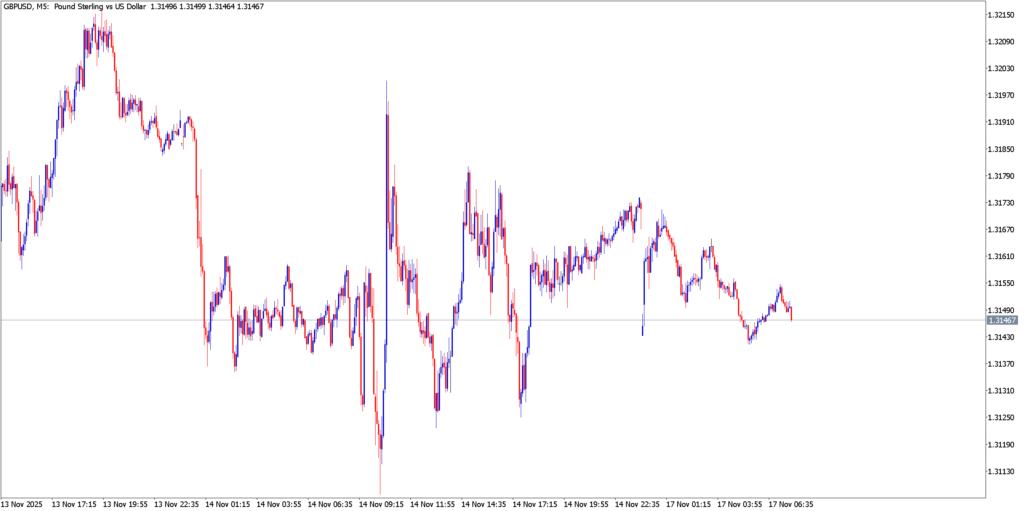

GBP/USD

Technical Analysis

GBP/USD spent most of the recent sessions stuck in a sideways crawl, reflecting indecision after the pair’s earlier retreat. The 5-minute chart shows cable confined to a narrow band roughly between $1.3120 and $1.3200. Multiple attempts to rally above $1.3200 were quickly capped – each minor uptick ran out of steam as sellers emerged around that resistance. At the same time, the 1.3120 floor held firm on dips; buyers repeatedly defended this support zone, preventing a breakdown. This tug-of-war has produced a flat, range-bound profile with progressively lower highs hinting at slight bearish pressure, but no decisive resolution either way. Essentially, momentum has evaporated – short-term moving averages on this timeframe have flattened out, and volatility is subdued (recent 5-day trading ranges for GBP/USD are modest at around 70–80 pips). The pair’s inability to break out suggests that traders are awaiting a fresh catalyst. A clear break below $1.3100 could open the door to a deeper decline (exposing the mid-$1.30s and possibly the $1.2950 region), whereas a push above $1.3200–1.3220 would signal that pound bulls are regaining traction. For now, the technical outlook is neutral-to-bearish in the very short term; the pound is drifting without conviction, and only a range breakout will provide direction.

Fundamental Analysis

On the fundamental front, the British pound’s struggles can be traced to a raft of disappointing UK economic data and growing policy uncertainty. Over the past week, markets digested news that the UK economy is barely treading water. The preliminary report for Q3 GDP showed an anemic 0.1% growth, falling short of expectations and underscoring near-stagnation. Other indicators flashed warning signs as well: the unemployment rate has been creeping higher, and notably it rose faster than forecasts, pointing to a cooling labor market. Industrial output is contracting – September’s industrial production fell roughly 2%, a much sharper drop than anticipated – highlighting weakness in the manufacturing sector. This steady drip of bad news has cast doubt on the UK’s resilience and is weighing on the pound. Traders are interpreting the data as a green light for the Bank of England to maintain a dovish stance. Indeed, with growth faltering and inflation pressures easing from earlier peaks, the BoE has little room (or reason) to hike rates further. Instead, discussion is gradually shifting to when rate cuts might come, especially if the economy continues to flirt with recession-like conditions. The mere hint of eventual BoE easing undermines GBP in forward-looking FX markets, especially against a dollar that, while off its highs, still enjoys yield support. Furthermore, fiscal uncertainty in Britain is adding another layer of risk. The UK Treasury has been struggling to finalize a budget, with debates raging over whether to raise taxes or cut spending to balance the books. This policy paralysis and political infighting are eroding confidence in the UK’s economic management. Currency traders loathe uncertainty, and the pound has felt the weight of that unpredictability as investors demand a risk premium. By contrast, across the Atlantic, the U.S. economy – while slowing – hasn’t delivered as starkly negative surprises, and U.S. fiscal policy (despite deficits) appears more steady in comparison. The result is a bias toward dollar strength against the pound, absent a compelling positive UK story. Looking ahead, sterling’s fortunes may turn if upcoming data or news surprises to the upside – for instance, traders will be closely watching the UK inflation report due mid-week. Any indication that price pressures are fading faster (or slower) than expected could swing BoE expectations and jolt GBP/USD out of its slumber. Similarly, improvement in UK retail sales or a breakthrough in the budget deadlock could help the pound find its footing. For now, however, the fundamental landscape favors a cautious outlook: the pound remains on the defensive, and without a shift in narrative, GBP/USD rallies are likely to be limited while the risk of a downside break lingers.

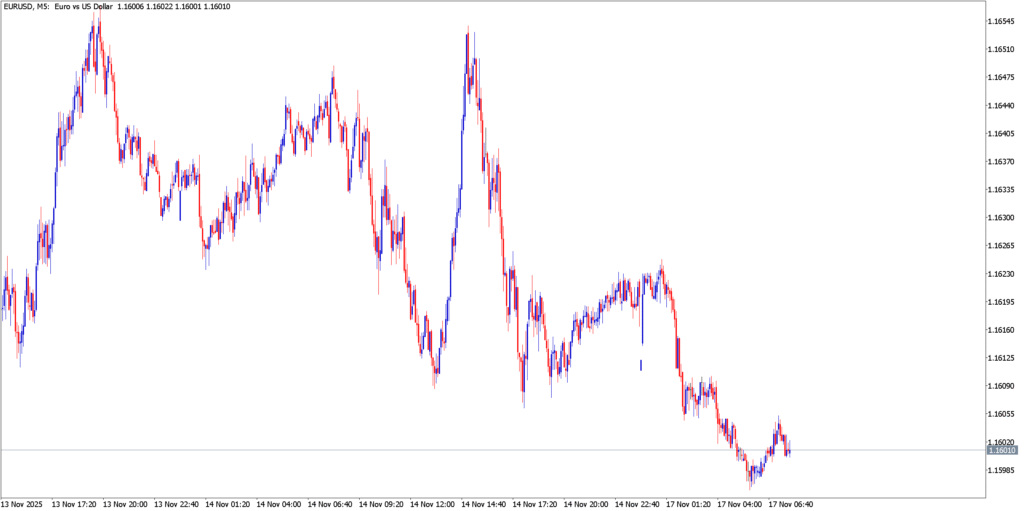

EUR/USD

Technical Analysis

EUR/USD has started to show signs of recovery after a prolonged downtrend in previous months. On the 5-minute chart, the euro staged a sharp rally late last week, bursting from the mid-$1.15s up to around $1.162 in a matter of hours. This surge broke the pair out of its earlier tight range and marked one of the strongest upside moves in weeks – a potential short-term trend reversal for the euro. After hitting that peak near $1.1620, the pair did undergo a modest pullback, retracing to about the $1.1560–1.1580 area. Notably, the retreat was orderly and relatively shallow: the euro found support above its prior resistance-turned-support zone (around mid-1.15s), and buyers stepped in quickly to arrest the decline. This behavior suggests the recent upswing was not a one-off spike but rather part of a nascent bullish structure. Indeed, the pair appears to be carving out a pattern of higher lows on the intraday charts. Short-term moving averages have flipped upward – for example, EUR/USD has been trading above its 50-period moving average on the M5 chart, which is now starting to slope up, signaling positive momentum. We’re also seeing early hints of bullish divergence on momentum indicators (such as RSI) as the pullback lost momentum while price held above its previous low. All of these technical cues point to a market that is trying to bottom out and rally. For the euro’s rebound to really gather steam, however, bulls need to clear the initial resistance around $1.1620–1.1650 (last week’s highs). A break above that zone would likely spur fresh buying, targeting the $1.1700 handle and beyond. On the downside, the $1.1550 level now acts as immediate support; a drop back below that could signal the euro’s recovery is faltering and put focus on the $1.1500 psychological level. At the moment, though, the technical tone has shifted cautiously optimistic in favor of the euro, as long as it continues to trade above its recent pivot lows.

Fundamental Analysis

From a fundamental standpoint, EUR/USD’s attempted comeback is being fueled by a mix of a softening US dollar and Europe’s comparatively steady (if unspectacular) fundamentals. Unlike the UK, the Eurozone hasn’t delivered much in the way of negative economic shocks lately. In fact, Eurozone GDP for Q3 2025 managed to grow about 0.2% quarter-on-quarter – a slow pace, but a notch better than the near-flat UK and avoiding contraction like Japan. This modest growth, coupled with a slight uptick from the previous quarter, suggests the Euro-area economy is avoiding the worst-case scenarios. Key economies like Germany and Italy were essentially flat in Q3, but not collapsing, and consumer spending has held up moderately. Meanwhile, Eurozone inflation has been gradually cooling from the highs of 2022-2024, easing pressure on the European Central Bank to keep tightening. The ECB has paused rate hikes since late summer, but importantly, it is not yet talking about rate cuts even as inflation retreats – policymakers have signaled a desire to see inflation sustainably near target before easing policy. This stance contrasts with rising speculation that the U.S. Federal Reserve could start cutting rates in 2026 if the U.S. economy slows significantly. The mere anticipation of a Fed policy reversal down the line has begun to cap the dollar’s strength broadly, benefiting the euro. In other words, the interest rate differential that had been strongly in the dollar’s favor is no longer widening; it may soon start to narrow if the Fed pivots while the ECB stays put for longer. That shift is a key undercurrent supporting EUR/USD’s rise from the lows. Additionally, the Eurozone’s current account and trade balances have improved compared to a year ago (helped by lower energy import costs and a weaker euro earlier this year boosting exports), which provides a fundamental tailwind for the currency. However, it’s not all clear skies for the euro. One emerging concern is trade tension between the US and EU. Just recently, reports surfaced that Washington is considering hefty tariffs (on the order of 15-20%) on a range of EU goods. Such protectionist moves, if implemented, could hurt European exports and investor sentiment, putting a damper on the euro’s recovery. Moreover, the Eurozone still faces headwinds like a struggling manufacturing sector and uncertainty in its eastern member states, which could limit how far euro optimism runs. In the near term, though, the balance of forces has shifted enough to give the euro a fighting chance. If upcoming data – such as Eurozone PMI surveys or the next inflation read – show an economy in decent shape and inflation coming under control, it will reinforce the case for the ECB to hold steady and for the euro to continue grinding higher. On the flip side, any resurgence of US economic strength or a spike in global risk aversion (which often sends traders back into the safe-haven dollar) could pause the EUR/USD rebound. For now, traders are cautiously leaning bullish on the pair, with an eye on the key $1.16+ resistance region to confirm the next leg up.

Market Outlook

As of mid-November 2025, the forex market presents a mixed landscape with each major pair telling a different story. USD/JPY stands out as the most dramatic narrative – a dollar seemingly unstoppable against the yen due to policy divergence and yield hunger, pushing into levels that invite speculation about how much further Japanese authorities will allow the yen to slide. This pair’s trajectory will be a central focus for traders, as any hint of BOJ policy adjustment or direct intervention could swiftly reverse the yen’s fortunes, while a continuation of the status quo likely means a march toward ¥155 and beyond. In contrast, GBP/USD is subdued, caught between opposing forces. The pound’s weakness reflects genuine economic troubles in the UK, yet its short-term range suggests neither side has had the conviction for a breakout. Going forward, catalysts like the UK’s upcoming inflation data or fiscal announcements could jar sterling from its range. A positive surprise – say inflation dropping faster, relieving pressure on consumers, or clarity on fiscal policy – might give GBP/USD a much-needed boost above $1.3200. Conversely, more gloomy news could finally crack that $1.3100 support and send the pair decisively lower into the $1.30–1.29 zone. EUR/USD, on the other hand, appears cautiously optimistic, with the euro leveraging a softer dollar narrative to climb off its lows. The key question is whether this rebound has legs. If U.S. economic indicators (like retail sales, jobless claims, or manufacturing data due in coming days) continue to hint at a slowdown, markets will firm up their bets that the Fed’s next move is a cut – a dollar-denting outlook that would favor further euro gains. Additionally, as long as the Eurozone avoids any major negative surprises, the euro should remain supported. Still, traders will keep an eye on external risks such as the brewing trade disputes and any shifts in risk sentiment that could quickly flip the script.

In summary, traders should brace for potential volatility as we progress through the week of Nov 17. Key levels to watch include roughly ¥155.0 on USD/JPY (a psychological ceiling where intervention talk would reach fever pitch) and support around the low ¥153s. For GBP/USD, the $1.3100 support and $1.3200 resistance are pivotal for breakout signals, aligning with our technical observations of the current range. EUR/USD bulls will look to $1.1650 then $1.1700 as upside hurdles in the coming days, with support at $1.1550 backing the newly formed uptrend. From a broader perspective, the US dollar’s next move is likely to be the common thread weaving through all these pairs’ outlooks. Any indication that the Fed might soften its stance sooner (due to economic slowdown or easing inflation) could relieve upward pressure on USD/JPY and propel EUR/USD and GBP/USD higher. Conversely, if U.S. data comes in hot or geopolitical jitters drive safe-haven flows, the dollar could reassert itself across the board – which might push USD/JPY further into uncharted territory while deepening the woes for the euro and pound. As always, maintaining a nimble approach is advisable: stay alert to news from central bankers and economic releases, and be ready to adjust positions as the forex narrative evolves throughout the week. In these turbulent market conditions, a clear game plan and careful risk management will be crucial for navigating the twists and turns in USD/JPY, GBP/USD, and EUR/USD.