Wednesday built on Tuesday’s reversal, but with an important nuance: the market was not just covering extreme dollar longs anymore, it was beginning to test whether the war premium had overshot. Reuters reported that the dollar declined for a second consecutive session as optimism about a Middle East ceasefire grew after President Trump said the U.S. could soon end its war with Iran and rely only on “spot hits” if necessary. The euro rose to around $1.1584, the dollar index fell to 99.67, and Brent crude dropped toward $101.

That made Wednesday a more convincing “anti-dollar” day than Tuesday, but still not a clean macro regime change. Reuters also reported that many strategists thought the dollar’s war-driven rebound would fade because its safe-haven appeal has eroded relative to gold and Treasuries, and because the greenback tends to weaken quickly when oil prices fall or conflict risks ease. The session therefore became a test of whether the market wanted to challenge the broader dollar narrative, not just trim it.

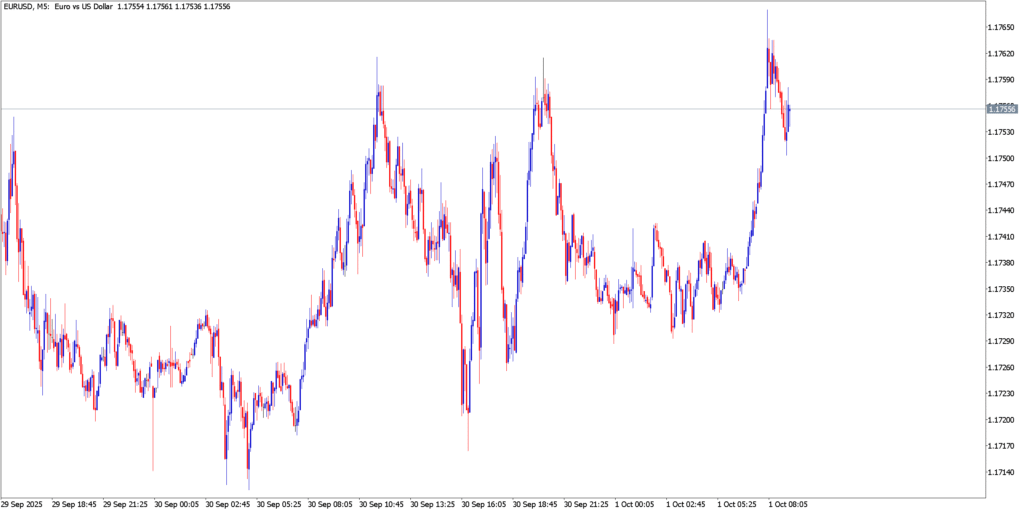

EUR/USD

Technical Analysis

EUR/USD looked steadier and more constructive than it had on Tuesday. The difference was not that the pair suddenly broke into a new uptrend, but that it was now able to hold gains more naturally rather than merely spike on short covering. That distinction matters. Relief rallies are often sharp and unstable; Wednesday’s euro move was more controlled, which suggested the market was becoming incrementally more comfortable rebuilding some non-dollar exposure.

Fundamental Analysis

Reuters reported that the euro strengthened as the dollar’s safe-haven appeal faded with de-escalation hopes and lower oil prices. That helped the euro because its biggest late-March problem had been the energy shock. Once Brent retreated, the market’s inflation-growth fear around Europe moderated slightly. It did not disappear, but it became less overwhelming. In that environment, EUR/USD could trade higher not because Europe looked strong, but because its most acute macro disadvantage was easing temporarily.

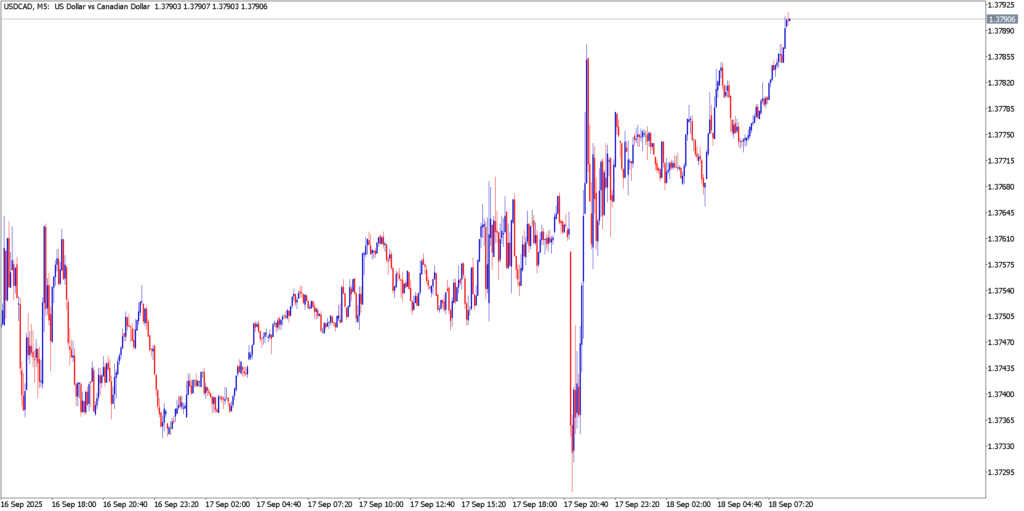

USD/CAD

Technical Analysis

USD/CAD fell, and unlike earlier in the week, the move felt more internally coherent. The loonie was finally able to benefit from a softer dollar environment without fighting such a strong haven premium. Technically, the pair looked like it was unwinding an overstretched rally rather than establishing a fresh upside base. That is the kind of action you often see when markets start rewarding currencies that had been unfairly dragged down by broad-based USD demand.

Fundamental Analysis

Reuters reported that the Canadian dollar gained to 1.3885 per U.S. dollar as Middle East optimism improved risk appetite, even though oil prices fell 2.2% and Canada’s manufacturing PMI weakened to 50.0. That is a subtle but important signal. The loonie’s gains came not from a stronger domestic story, but from the fading of the dollar’s panic premium. Reuters also noted that investors saw Canada as a potential longer-run beneficiary of postwar oil and gas investment. So USD/CAD became one of Wednesday’s clearest “less fear, less dollar” trades.

USD/JPY

Technical Analysis

USD/JPY slipped again as the market reassessed the need for heavy dollar positioning and as the pair remained capped by the same political sensitivity around 160. Technically, it looked more like a controlled retracement than a full structural reversal, which made sense: the broader trend had been strong, but the pair was overstretched and sitting near a zone where officials were already uncomfortable.

Fundamental Analysis

Reuters reported the yen strengthened modestly to around 158.85 per dollar as the U.S. dollar weakened broadly. This was not just a dollar story, though. The yen had a natural advantage in a session where war intensity looked less threatening and U.S. yields were not the dominant driver. As the pressure of relentless dollar buying eased, traders were more willing to respect the possibility that Tokyo might not tolerate another aggressive run through 160 without stronger justification.

Market Outlook

Wednesday was the strongest challenge yet to the late-March dollar regime. The greenback had now fallen for two straight sessions, oil had eased, and markets were openly discussing whether the war premium in FX had been too aggressively priced. Still, none of this yet amounted to a durable anti-dollar thesis; it remained conditional on conflict de-escalation and lower energy prices holding.

Check out our other forex market analysis: