Tuesday’s session marked one of the strongest days for the U.S. dollar in several weeks as rising Treasury yields and shifting Federal Reserve expectations forced traders to reassess positions established during May’s anti-dollar trend.

Throughout much of the month, markets had grown increasingly comfortable pricing in eventual Federal Reserve easing later in the year. Softer inflation expectations, stable commodity prices, and relatively contained geopolitical risks encouraged investors to reduce defensive dollar exposure. However, that narrative came under pressure on May 26.

U.S. Treasury yields moved sharply higher across the curve, with investors increasingly questioning whether the Fed would be able to ease policy as quickly as previously anticipated. Recent U.S. economic indicators continued showing resilience, particularly in labor market conditions and consumer spending. While inflation has moderated significantly from its peak levels, policymakers have repeatedly emphasized that the final stage of disinflation could prove more difficult.

Globally, risk sentiment also became slightly more defensive. Concerns surrounding Chinese growth continued to linger as property-sector weakness remained unresolved, while investors monitored ongoing geopolitical uncertainty in the Middle East. Although tensions around Iran and regional shipping routes remained well below crisis levels, they continued providing a background layer of uncertainty that prevented aggressive risk-taking.

The result was a broad-based dollar recovery that pressured European currencies, lifted USD/JPY, and weighed heavily on gold.

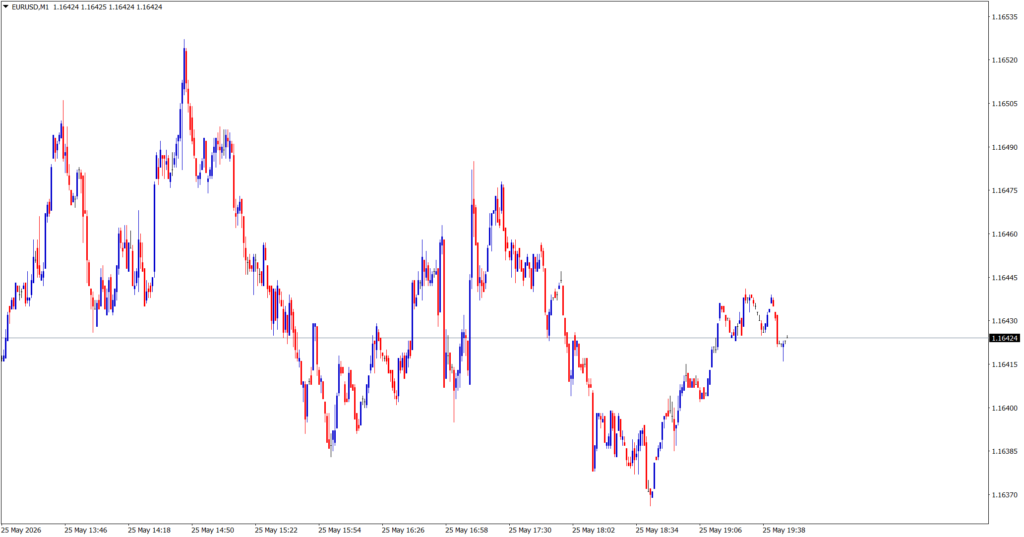

EUR/USD

Technical Analysis

EUR/USD experienced one of its weakest sessions in nearly two weeks as buyers failed to defend recent highs. The pair broke lower through short-term support levels and spent most of the session trading near the bottom of its recent range.

From a technical perspective, the move represents the most serious challenge to the euro’s May recovery trend so far. While the broader medium-term structure remains constructive, momentum indicators have begun rolling over from previously elevated levels.

The pair now appears vulnerable to a deeper retracement if dollar strength continues during the remainder of the week.

Fundamental Analysis

The euro came under pressure primarily because of widening interest-rate differentials.

As Treasury yields rose, investors became less confident that the Federal Reserve would begin easing aggressively during the second half of 2026. That directly strengthened the dollar.

Meanwhile, the European economic picture remains mixed. While inflation across the eurozone has continued moderating, growth remains sluggish in several key economies. Germany, the region’s largest economy, continues facing manufacturing weakness and soft industrial demand. Recent data has shown stabilization, but not enough to generate confidence that Europe can significantly outperform the United States.

The ECB also faces a difficult balancing act. While inflation pressures have eased, economic growth remains weak enough to justify a more accommodative stance later in the year. That contrasts with the Fed’s increasingly cautious approach and helped drive EUR/USD lower during Tuesday’s session.

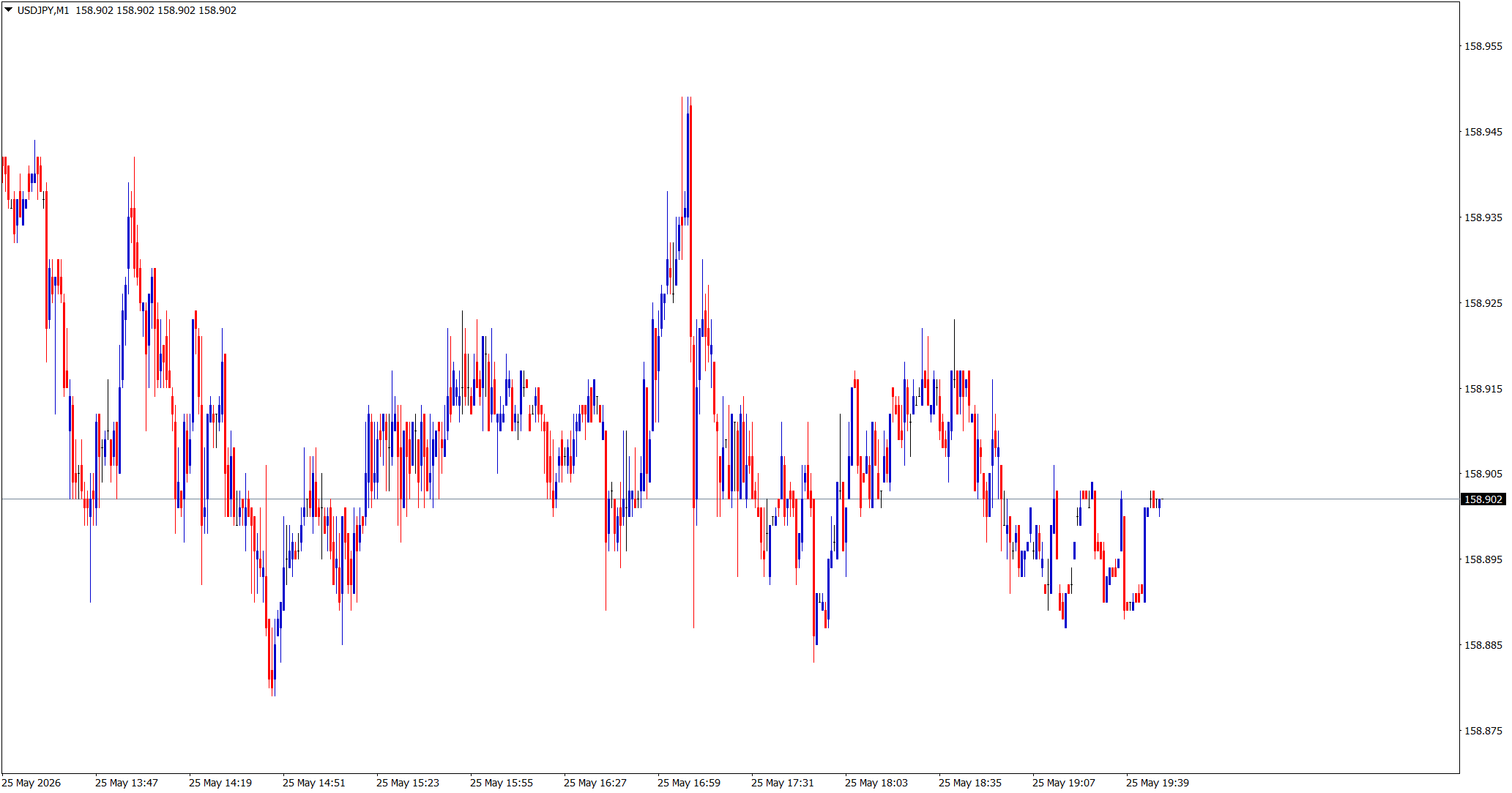

USD/JPY

Technical Analysis

USD/JPY posted a strong recovery and climbed steadily throughout the session as buyers returned aggressively following several weeks of corrective weakness.

The pair successfully defended recent support levels and regained important technical territory that had been lost earlier in May. Momentum indicators improved significantly, suggesting that bearish pressure has weakened in the short term.

However, resistance remains substantial near recent highs, and traders remain cautious about chasing the pair too aggressively given ongoing intervention concerns from Japanese authorities.

Fundamental Analysis

The primary driver behind Tuesday’s rally was the sharp rise in U.S. Treasury yields.

USD/JPY remains one of the most yield-sensitive currency pairs in the world. When U.S. yields rise while Japanese yields remain relatively low, capital naturally flows toward dollar-denominated assets.

Although the Bank of Japan has gradually moved away from its ultra-loose policy stance over the past year, Japanese rates remain extremely low compared with U.S. rates. That continues supporting the carry-trade dynamic that has dominated USD/JPY for much of the past several years.

At the same time, recent comments from Japanese officials regarding currency stability have done little to alter the market’s underlying view. Traders still believe intervention risk exists, but only if moves become excessively rapid or disorderly.

As a result, rising Treasury yields overwhelmingly dominated the session and pushed USD/JPY higher.

XAU/USD

Technical Analysis

Gold experienced significant selling pressure and posted one of its weakest sessions of the month. After repeatedly finding support during recent pullbacks, XAU/USD finally broke lower as buyers stepped aside.

The metal failed to sustain key support levels and spent much of the session trading defensively. Momentum indicators have turned lower, suggesting that bullish enthusiasm has weakened in the near term.

While the longer-term uptrend remains intact, Tuesday’s price action signals that gold may require fresh catalysts before resuming higher.

Fundamental Analysis

Gold’s weakness was driven by a combination of factors.

First, rising Treasury yields increased the opportunity cost of holding non-yielding assets like gold. This remains one of the strongest negative drivers for precious metals.

Second, the stronger dollar created additional headwinds. Since gold is priced in dollars, a stronger greenback typically makes the metal more expensive for international buyers and reduces demand.

Third, although geopolitical tensions remain present, they have not escalated enough to trigger significant safe-haven flows. Markets continue viewing Middle East risks as manageable rather than systemic.

However, gold still retains several longer-term supportive themes:

- Central-bank buying remains historically strong.

- Global debt concerns continue supporting diversification demand.

- Many investors still expect eventual Fed easing later in the year.

These factors may limit downside pressure even if short-term weakness persists.

Market Outlook

Tuesday’s session represented a meaningful shift in market psychology.

For much of May, traders were comfortable betting against the dollar based on expectations that:

- inflation would continue falling,

- yields would gradually decline,

- and Fed easing would become increasingly likely.

May 26 challenged that narrative.

The combination of:

- stronger Treasury yields,

- resilient U.S. economic data,

- and cautious Fed messaging

reminded investors that the path toward lower rates may not be as straightforward as previously assumed.

Looking ahead, markets will continue monitoring:

- Treasury yield movements

- Federal Reserve commentary

- Eurozone growth data

- Chinese economic developments

- Middle East geopolitical risks

If yields continue rising, the dollar could extend gains further.

However, if incoming data begins supporting renewed easing expectations, the anti-dollar trend that dominated much of May could quickly re-emerge.

For now:

- EUR/USD faces growing downside pressure.

- USD/JPY has regained bullish momentum.

- Gold is experiencing its most significant correction in weeks.

- The dollar has re-established itself as the market’s preferred currency whenever yields move higher.