Wednesday’s session was a pause day, but not a quiet one in terms of market significance. After the dollar regained control on May 26 through higher Treasury yields and renewed concern that the Federal Reserve may have to stay restrictive for longer, May 27 became a session of digestion rather than continuation.

World equities held close to record highs, but major markets including the S&P 500, Treasuries, and the dollar were largely steady as investors weighed conflicting signals around a possible U.S.-Iran peace deal and waited for the next U.S. inflation catalyst. Reuters described the day as a “pause before PCE,” with traders focused on Thursday’s PCE inflation data and GDP figures. That setup mattered because the recent dollar rebound was highly dependent on yields and inflation expectations; without new confirmation, traders were reluctant to extend the move aggressively.

At the same time, the broader dollar story remained supportive. Reuters reported that investors were increasingly looking for the dollar to break higher as the Fed shifted more directly toward fighting inflation risks tied to higher oil prices and a resilient U.S. economy. Rising inflation expectations from the Iran war and Strait of Hormuz disruptions had increased demand for higher yields, widening the dollar’s advantage over lower-yielding peers.

The key market tension was therefore simple: the dollar had a strong macro story, but traders needed PCE confirmation before adding heavily to it.

EUR/USD

Technical Analysis

EUR/USD stabilized after Tuesday’s decline, trading in a narrower range as sellers paused near short-term support. The pair did not recover strongly, but it also avoided a deeper breakdown, suggesting that traders were unwilling to press euro shorts before the U.S. inflation data.

Technically, the pair remained under pressure after losing momentum earlier in the week. The euro’s prior recovery structure was still intact on the broader chart, but the short-term tone had clearly shifted from constructive to cautious. The pair’s inability to reclaim recent highs suggested that bullish conviction had faded, while the lack of a decisive break lower showed that sellers were waiting for confirmation from PCE.

In practical terms, EUR/USD entered a holding pattern. A hotter U.S. inflation reading would likely expose the pair to deeper downside, while softer data could quickly revive the anti-dollar trend that dominated much of May.

Fundamental Analysis

The euro remained caught between improving geopolitical sentiment and a stronger dollar rates narrative. On one hand, cautious optimism around a possible U.S.-Iran deal and potential reopening of the Strait of Hormuz helped reduce some pressure on energy-importing economies like the eurozone. Lower energy risk usually supports the euro because it reduces imported inflation pressure and improves the growth outlook.

On the other hand, the U.S. dollar’s yield advantage remained a major obstacle. Reuters noted that investors expected the dollar could break higher as the Fed focused on inflation risks, with resilient U.S. growth and higher Treasury yields supporting the greenback.

That left EUR/USD without a strong independent bullish driver. The euro could stabilize when dollar buying paused, but it lacked the momentum to lead unless U.S. yields moved lower or geopolitical de-escalation became more concrete.

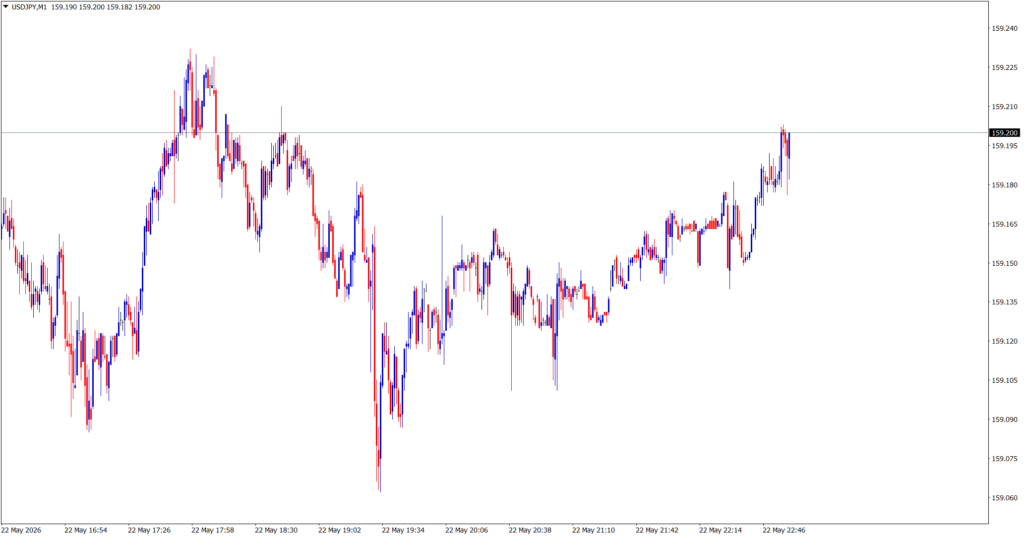

USD/JPY

Technical Analysis

USD/JPY paused after Tuesday’s strong rebound, holding most of its gains but failing to extend decisively higher. The pair remained elevated, but price action was more hesitant as traders waited for U.S. inflation data and watched whether yields could continue rising.

Technically, the pair remained supported above recent corrective lows. Tuesday’s rally had repaired some of the short-term damage created earlier in May, but Wednesday’s lack of follow-through showed that buyers were not yet fully comfortable chasing the pair higher.

The area near 160 remained psychologically and politically sensitive. Even when the yield backdrop supports USD/JPY, traders remain aware that Japanese officials may become more vocal if the pair rises too quickly or trades disorderly near intervention-sensitive levels.

Fundamental Analysis

USD/JPY remained one of the clearest expressions of the U.S. yield story. When Treasury yields rise, the dollar gains a stronger carry advantage over the yen, especially because Japanese yields remain far lower despite gradual Bank of Japan normalization.

However, Wednesday’s steadier yield environment limited additional upside. Reuters’ market commentary noted that major markets were largely steady as investors waited for PCE data, meaning USD/JPY lacked a fresh rates catalyst.

The yen also remains tied to global risk and energy dynamics. Japan is highly exposed to imported energy, so the Iran war and Strait of Hormuz disruption can weigh on the yen through higher import costs. But if peace-deal optimism strengthens, that pressure eases. This creates a mixed backdrop: USD/JPY is supported by U.S. yields, but capped by intervention risk and shifting oil expectations.

XAU/USD

Technical Analysis

Gold was one of the day’s most important markets. XAU/USD fell to a two-month low, confirming that the precious metal remained under pressure from the combination of high yields and a firmer dollar. Spot gold dropped 1.3% to $4,447.71 per ounce, while U.S. gold futures settled 1.2% lower.

Technically, this was a damaging session for gold’s short-term structure. The break to a two-month low showed that buyers were not defending prior support zones with the same conviction seen earlier in the year. Momentum remained negative, and the metal looked vulnerable to further downside if PCE reinforced the higher-for-longer Fed narrative.

However, the late-session easing of losses after reports that Iran may restore shipping lanes suggested gold was not completely abandoned. The metal remained sensitive to both rates and geopolitical headlines.

Fundamental Analysis

Gold’s weakness reflected the unusual nature of the current inflation shock. Normally, geopolitical tension and inflation fears can support gold. But this time, the dominant market interpretation was that war-driven inflation could force the Fed to stay restrictive or even consider another rate hike. That is negative for gold because higher yields increase the opportunity cost of holding a non-yielding asset.

Reuters reported that gold fell as inflation fears from the U.S.-backed war with Iran fueled expectations of tighter U.S. monetary policy, with investors watching PCE for further policy clues. Minneapolis Fed President Neel Kashkari also emphasized the need to contain inflation.

So gold was not falling because geopolitical risk disappeared. It was falling because the market believed geopolitical risk was inflationary enough to support yields and hurt non-yielding assets. That made XAU/USD one of the clearest symbols of the week’s macro tension.

Market Outlook

May 27 was a transition session. The dollar did not extend sharply, but the broader setup still leaned in its favor as long as yields stayed elevated and inflation risks remained alive.

The next decisive move depended heavily on PCE and U.S.-Iran headlines. A hotter inflation reading would likely support the dollar, pressure EUR/USD, lift USD/JPY, and keep gold under pressure. A softer or in-line print, especially combined with ceasefire optimism, could trigger a reversal in the dollar and allow gold to stabilize.

For now:

- EUR/USD remained vulnerable but not broken.

- USD/JPY held its yield-driven recovery.

- XAU/USD was under clear pressure from rate-hike expectations.

- The dollar’s near-term path depended on whether PCE confirmed or challenged the inflation-risk narrative.