Friday’s session concluded one of the most fascinating trading weeks of 2026, as the market transitioned from celebrating geopolitical de-escalation earlier in the week to focusing almost entirely on Federal Reserve policy, Treasury yields, and the resilience of the U.S. economy.

At the beginning of the week, investors were overwhelmingly optimistic following the announcement of a framework agreement between the United States and Iran. Oil prices collapsed, inflation fears eased, and markets immediately began pricing a friendlier environment for risk assets. The euro, pound, and commodity-linked currencies all rallied sharply as traders anticipated lower energy costs, weaker inflation pressures, and a potentially less aggressive Federal Reserve.

However, by Friday, that narrative had largely faded.

Instead, investors were forced to confront a different reality: the U.S. economy remains remarkably resilient.

The week’s Federal Reserve meeting proved to be the turning point. Although policymakers left interest rates unchanged, officials made it clear that inflation risks remain elevated and that recent declines in energy prices alone are not sufficient to guarantee a smooth return toward the Fed’s target. Several policymakers emphasized that labor markets remain strong, consumer demand remains healthy, and inflation progress has slowed compared to earlier expectations.

Markets responded by pushing Treasury yields higher throughout the second half of the week.

The benchmark 10-year Treasury yield climbed toward recent highs, while shorter-term yields reflected reduced expectations for near-term rate cuts. Interest-rate futures began pricing a much shallower easing cycle than investors anticipated only a few weeks ago.

At the same time, geopolitical uncertainty did not disappear entirely.

While the U.S.-Iran agreement remained intact, reports emerged that negotiations had slowed and several implementation details remained unresolved. Simultaneously, renewed tensions between Israel and Hezbollah reminded investors that Middle East risks have not completely vanished.

The combination of:

- higher Treasury yields

- resilient U.S. economic data

- reduced expectations for Fed easing

- lingering geopolitical uncertainty

created a highly supportive environment for the dollar.

As a result, the greenback finished the week near its strongest levels in over a month, while the yen approached fresh multi-decade lows and European currencies surrendered much of their earlier gains.

EUR/USD

Technical Analysis

EUR/USD spent Friday under consistent pressure and closed near the bottom of its weekly range.

After beginning the week with strong upside momentum, the pair gradually reversed course following the Federal Reserve meeting. Friday’s price action confirmed that the euro was unable to sustain its earlier breakout, with sellers regaining control across multiple timeframes.

From a technical perspective, the pair has now returned toward an important support zone that has repeatedly acted as a battleground between buyers and sellers throughout the second quarter.

The failure to hold above recent resistance levels is significant because it suggests that bullish momentum has weakened considerably.

Several technical indicators also support this view:

- Daily RSI has rolled over from previously bullish territory.

- MACD momentum continues to soften.

- Short-term moving averages are beginning to flatten.

The broader medium-term structure remains constructive, but the immediate outlook has clearly deteriorated.

Should Treasury yields continue climbing next week, EUR/USD could face additional downside pressure toward the lower end of its spring trading range.

Fundamental Analysis

The euro’s weakness was driven primarily by widening yield differentials.

Throughout much of the first half of 2026, investors believed the Federal Reserve would eventually begin a meaningful easing cycle while the European Central Bank remained relatively cautious. That narrative helped support EUR/USD.

However, recent developments have challenged that assumption.

The Fed’s latest communication reinforced the idea that U.S. policymakers remain concerned about inflation persistence. While energy prices have fallen sharply since the Iran agreement, core inflation pressures remain stubborn enough to justify maintaining restrictive policy.

At the same time, Europe’s growth outlook remains mixed.

Germany continues struggling with weak manufacturing activity, France faces slower business investment, and broader eurozone growth remains significantly weaker than the United States.

While lower oil prices certainly help Europe, they do not completely solve the region’s structural growth challenges.

Investors increasingly recognize that the ECB may eventually face greater pressure to support growth than the Federal Reserve.

This has shifted relative policy expectations back in favor of the dollar.

Another important factor is global capital flows.

Higher Treasury yields continue attracting international investment into U.S. fixed-income markets. Even investors who remain cautious about the long-term dollar outlook are finding it difficult to ignore the attractive yield advantage available in the United States.

As a result, EUR/USD ended the week on defensive footing despite generally positive developments in energy markets.

USD/JPY

Technical Analysis

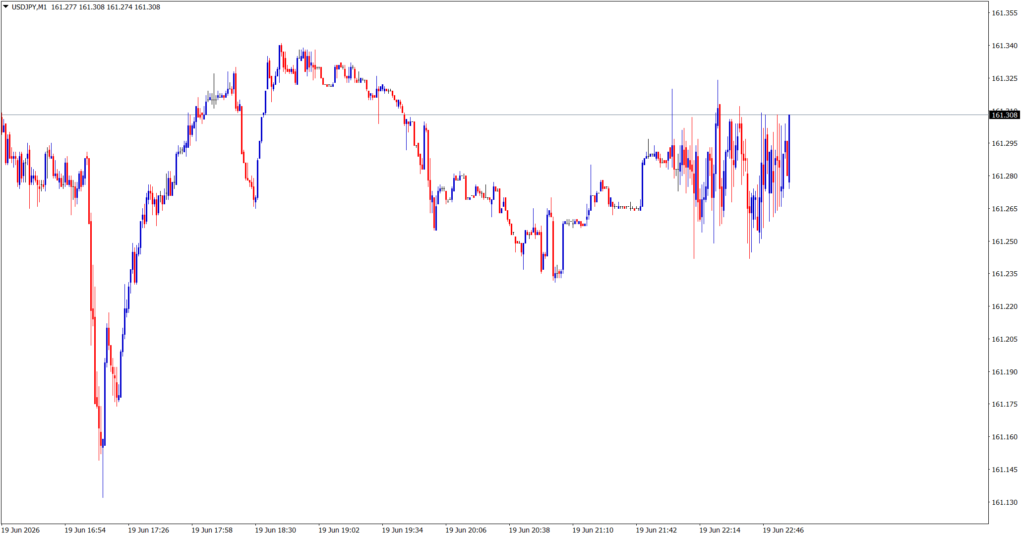

USD/JPY was unquestionably one of the most important markets on Friday.

The pair surged toward the 161 area and approached levels not seen in decades. Momentum remained overwhelmingly bullish throughout the session, with every intraday pullback attracting fresh buyers.

Technically, the pair has completely reversed the corrective decline that occurred earlier in June.

The breakout above 160 was particularly important because that level has repeatedly served as both a psychological barrier and a potential intervention trigger.

Key technical observations include:

- Strong upward momentum across daily and weekly charts.

- Consistent support from moving averages.

- No meaningful signs of trend exhaustion yet.

- Strong volume accompanying recent advances.

However, there is one major caveat.

The higher USD/JPY rises, the greater the risk of intervention from Japanese authorities.

Traders remain highly aware that the Ministry of Finance has previously intervened at similar levels when yen weakness became excessively rapid.

For now, however, yield differentials continue overwhelming intervention concerns.

Fundamental Analysis

The fundamental story behind USD/JPY remains remarkably straightforward.

Treasury yields are rising.

Japanese yields are not.

That gap continues driving capital toward the dollar.

The Bank of Japan has gradually moved away from its ultra-accommodative policies, but Japanese interest rates remain dramatically lower than those in the United States.

Consequently, global investors continue using the yen as a funding currency for carry trades.

Every time U.S. yields rise, the attractiveness of those trades increases.

Friday’s move was further amplified by the week’s strong U.S. labor-market data and hawkish Fed messaging.

Investors increasingly believe that U.S. rates could remain elevated well into 2027.

In contrast, the Bank of Japan remains constrained by:

- weak domestic growth

- high public debt levels

- fragile consumer demand

This policy divergence remains one of the strongest themes in global FX markets.

At the same time, Japan’s energy-import dependence creates another challenge.

Although oil prices have fallen recently, the country remains highly exposed to global commodity fluctuations. Any renewed geopolitical tensions could quickly worsen Japan’s trade balance and place additional pressure on the yen.

As a result, USD/JPY remains one of the clearest expressions of both U.S. economic strength and global policy divergence.

GBP/USD

Technical Analysis

GBP/USD continued weakening and ended the week near session lows.

The pair failed to sustain the bullish breakout achieved earlier in the week and instead drifted steadily lower as dollar demand increased.

Technically, sterling remains trapped within a broad consolidation pattern that has dominated much of the second quarter.

Recent price action suggests:

- buyers are becoming less aggressive

- resistance remains difficult to overcome

- downside risks are increasing

Momentum indicators have weakened noticeably since the start of the week.

While the broader structure remains intact, sterling clearly lost leadership among major currencies during Friday’s session.

Fundamental Analysis

The pound faced challenges from both domestic and international developments.

Internationally, the same factors supporting the dollar against the euro also weighed on sterling:

- higher Treasury yields

- hawkish Fed expectations

- strong U.S. economic data

However, sterling faced an additional obstacle.

Political uncertainty within the United Kingdom has begun re-emerging as a market concern.

Questions surrounding the stability of Prime Minister Keir Starmer’s government, combined with debates over fiscal policy and public spending, have introduced a modest political risk premium into sterling assets.

While these concerns are nowhere near crisis levels, they reduce investors’ willingness to aggressively buy the pound during periods of dollar strength.

Meanwhile, the Bank of England remains in a difficult position.

Inflation has eased substantially, but economic growth remains sluggish.

This creates a policy dilemma:

- ease too quickly and inflation risks return

- stay restrictive too long and growth weakens further

Compared to the relatively strong U.S. economy, the UK currently offers fewer compelling reasons for international investors to increase exposure.

That imbalance contributed to sterling’s underperformance throughout Friday’s session.

Market Outlook

Friday’s trading confirmed that the market’s primary focus has shifted decisively back toward monetary policy.

Earlier in the week, investors were focused on:

- the Iran agreement

- falling oil prices

- improving risk sentiment

By the end of the week, attention had returned to:

- Federal Reserve policy

- Treasury yields

- labor-market resilience

- inflation persistence

This transition matters because yield differentials remain one of the most powerful drivers in foreign exchange markets.

Looking ahead, traders will closely monitor:

Federal Reserve Expectations

The key question is whether incoming U.S. data continues supporting the Fed’s cautious stance.

If inflation remains sticky and labor markets remain strong, expectations for rate cuts could continue being pushed further into the future.

That would remain supportive for the dollar.

Japanese Intervention Risk

USD/JPY is entering increasingly dangerous territory.

Every move higher increases the probability of verbal or actual intervention by Japanese authorities.

The market currently believes yields matter more than intervention threats.

Whether that assumption remains correct will be tested soon.

European Growth Concerns

Lower energy prices help Europe, but they do not eliminate structural growth challenges.

Investors will continue evaluating whether the eurozone can generate enough economic momentum to offset the dollar’s yield advantage.

UK Political Developments

Sterling may become increasingly sensitive to domestic political headlines if uncertainty continues growing.

This could amplify moves generated by broader dollar trends.