Friday delivered the week’s macro verdict: US inflation came in cooler than expected, with the CPI rising 0.2% vs. 0.3% forecast, reinforcing the view that the Fed can remain patient now but still cut later in 2026.

The FX reaction was restrained and tactical: the dollar was broadly flat-to-soft, while the yen was set for its strongest weekly gain in roughly 15 months, reflecting both the week’s Japan-side repricing and the post-CPI yield drift lower.

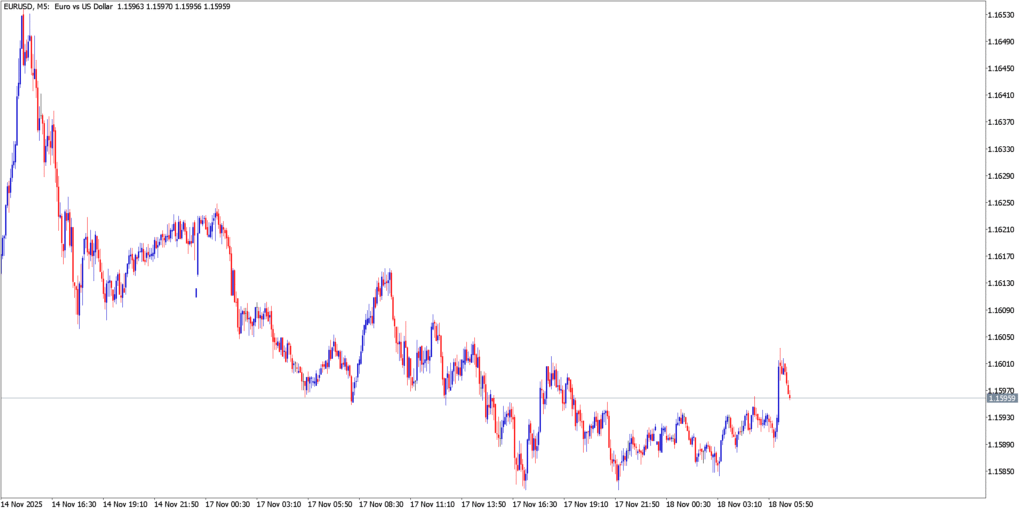

EUR/USD

Technical Analysis

EUR/USD held firm near its established range highs. The key technical takeaway was resilience: despite midweek USD rebound attempts, the pair maintained support and avoided a deeper retracement, suggesting underlying demand remained intact.

Fundamental Analysis

Cooler CPI keeps easing “in play” later this year, and that undermines sustained USD rallies. Reuters emphasized that while there’s little urgency for immediate Fed action, the inflation tone still supports cuts later, enough to keep the dollar from regaining strong momentum.

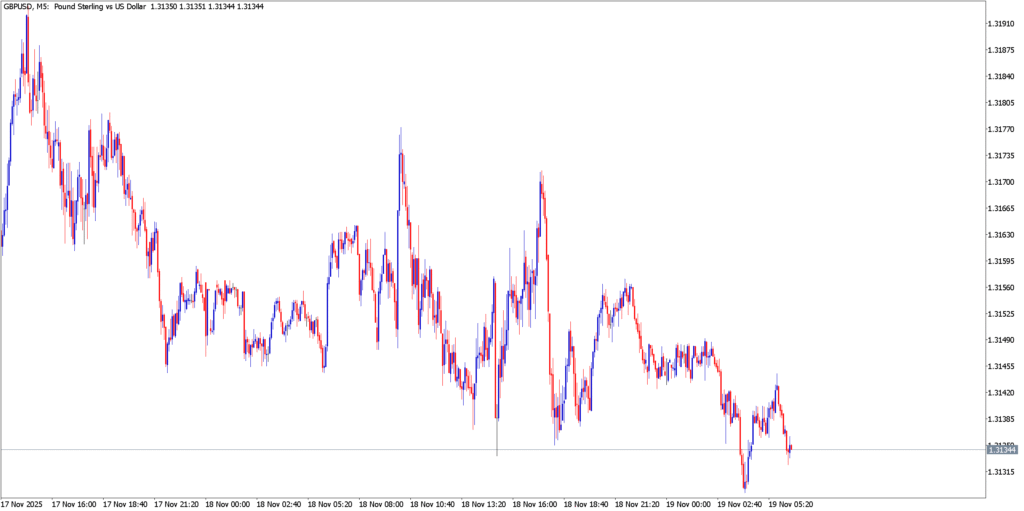

GBP/USD

Technical Analysis

GBP/USD held steady to mildly firm, behaving like EUR/USD: stable support, limited downside, and a market reluctant to chase USD strength after CPI.

Fundamental Analysis

Sterling’s move was mostly a dollar story. Cooler inflation reduces the pressure for “higher for longer,” which helps GBP/USD stabilize even without UK-driven catalysts.

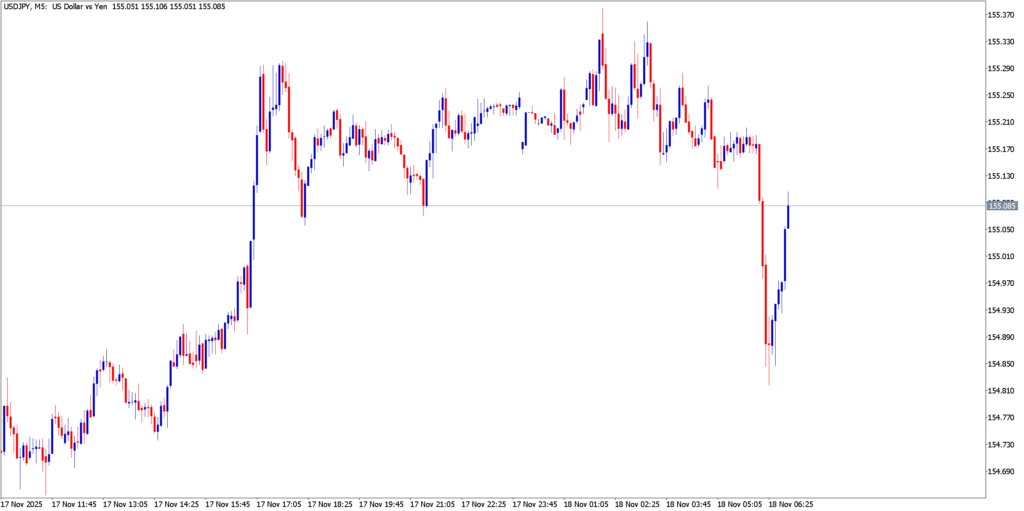

USD/JPY

Technical Analysis

USD/JPY remained capped, with the yen still dictating the pair’s behavior. Intraday movement looked choppy but biased lower across the week, consistent with a durable yen bid.

Fundamental Analysis

The yen’s weekly performance was the headline: Reuters noted it was poised for its strongest weekly gain in 15 months, supported by improved confidence after Japan’s election outcome and reduced fiscal fear, plus a CPI-driven environment that didn’t restore USD yield dominance.

Market Outlook

The Feb 9–13 week ended with a clearer hierarchy of drivers:

- USD: sensitive to inflation and yield drift; strong labor helps, but cooler inflation caps rallies.

- JPY: structurally supported by post-election repricing and confidence; USD/JPY remains the most reactive pair.

- EUR/USD & GBP/USD: range-resilient as long as USD fails to reassert yield dominance.

With that, the market moved into mid-February with USD softer, yen stronger, and major pairs technically coiled for the next macro catalyst.