Midweek forex trading brought high drama despite modest price swings. On Wednesday, November 12, 2025, the US Dollar found itself on shaky footing as traders braced for a potential end to Washington’s protracted budget showdown. Major currency pairs responded with a mix of consolidation and reversals: the Euro clung to multi-week highs, the British Pound’s early strength evaporated, and the Canadian Dollar held its ground near a key threshold. Investors navigated a swirl of cross-currents – from dovish Fed expectations to political optimism – leaving the forex market poised but undecided as the session closed.

EUR/USD

Technical Analysis

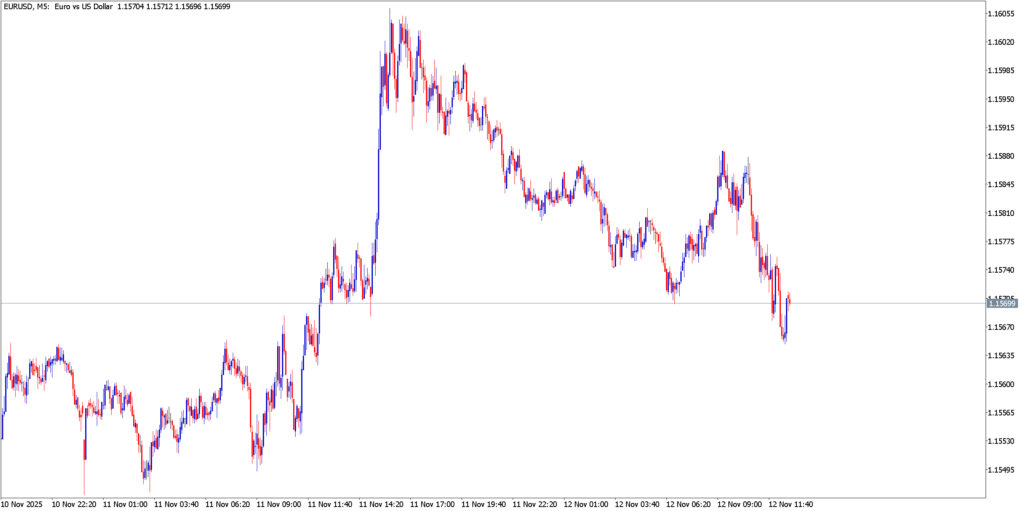

EUR/USD spent Wednesday in consolidation mode on the 5-minute chart, trading in a tight range below the 1.1600 handle. The pair failed to break above Tuesday’s peak (just over 1.1600), instead stalling near that resistance and retreating slightly. An early attempt to push higher was met with selling pressure around the two-week high region, resulting in a sideways drift for most of the day. Intraday price action formed a modest range roughly between 1.1570 support and 1.1600 resistance, with neither level decisively breached. This lack of follow-through in either direction signaled indecision – a classic range-bound pattern where short-term moving averages flattened out and momentum oscillators offered few clear signals. In sum, the Euro’s technical picture was one of hesitation, as bulls paused after recent gains and bears lacked the strength to force a deeper pullback.

Fundamental Analysis

The Euro’s firm footing came amid a largely neutral fundamental backdrop. Early in the day, data confirmed easing inflation in the Eurozone’s powerhouse economy – Germany’s October consumer prices held steady at low levels – reinforcing the view that the European Central Bank’s policy stance would remain steady. Across the Atlantic, the Dollar was on the defensive after a string of soft U.S. indicators. In particular, a surprise decline in U.S. private employment (reported earlier in the week) underscored a cooling labor market, bolstering bets that the Federal Reserve could cut interest rates in December. This prospect kept the Dollar under pressure, which helped EUR/USD stay elevated. However, traders were equally wary of looming events. All eyes were on Washington, where Congress was poised to vote on a stopgap funding bill to finally reopen the government after a record shutdown. Caution prevailed as currency markets awaited the outcome of that political saga. Additionally, a slew of Fed officials scheduled to speak injected uncertainty – market participants were listening for any hint on future monetary policy but received no major surprises by midweek. The net effect was a balancing act: mildly Euro-positive factors (weaker USD sentiment and decent Eurozone data) offset by a wait-and-see mood ahead of U.S. fiscal and policy news. This fundamental equilibrium translated into the Euro’s range-bound performance on the day.

GBP/USD

Technical Analysis

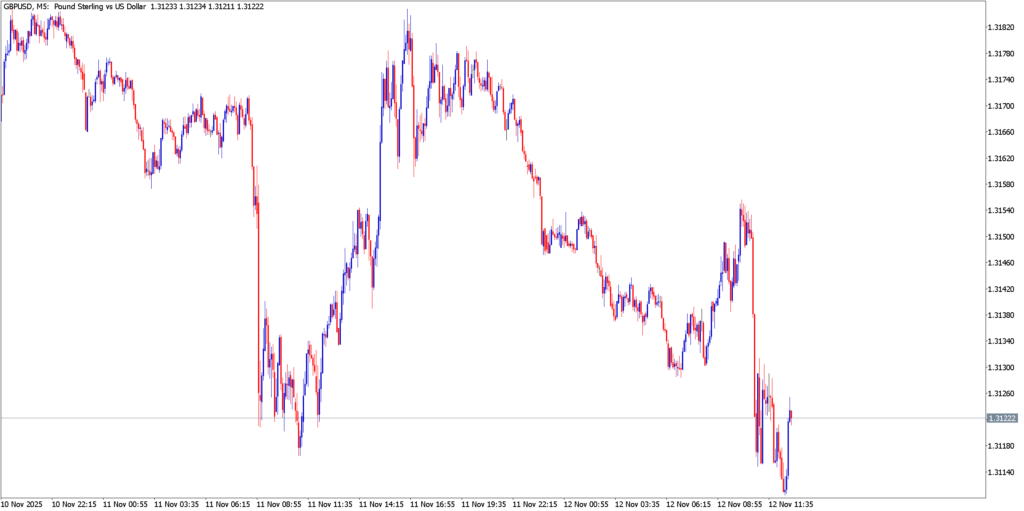

The British Pound initially extended its bounce against the Dollar on Wednesday, but bullish momentum faded as the day progressed. On the intraday M5 chart, GBP/USD climbed during the Asian and early European sessions, reaching toward the mid-1.3100s. This early strength saw the pair testing near the week’s highs around the 1.3150 level. However, a clear ceiling emerged in that zone – the pound failed multiple attempts to sustain gains above roughly 1.3140, hinting at a double-top pattern on the short-term timeframe. As European trading wore on, the pair reversed course. A wave of Dollar buying and profit-taking on long sterling positions knocked GBP/USD lower, erasing its intraday gains. By mid-session, the rate had slipped back toward 1.3100, a level which offered minor support. The retreat from 1.3150 to 1.3100 effectively snapped the pound’s recovery and put the pair back into its prior range. Short-term indicators flipped bearish during this pullback – for instance, momentum oscillators on the M5 chart rolled over from overbought conditions. Still, the 1.3100 handle held by the U.S. afternoon, preventing a deeper sell-off. In summary, GBP/USD’s technical tone turned choppy, with an early rally giving way to a mid-day reversal. The failure at resistance and subsequent dip signaled that the pair remained in consolidation, lacking the catalyst for a sustained breakout above the 1.3170 area or below 1.3080 in the intraday timeframe.

Fundamental Analysis

Fundamentally, the Pound’s mixed performance reflected crosswinds from home and abroad. On one hand, the UK currency was grappling with downbeat domestic data. Earlier in the week, Britain’s labor market reports revealed weakness – rising unemployment and slower wage growth pointed to a cooling economy. These soft figures have strengthened the case that the Bank of England might lean dovish, with some investors even entertaining rate cut bets for early 2026. This backdrop made traders cautious about pushing GBP much higher. On the other hand, global factors provided an initial boost to sterling. The overall market mood was cautiously optimistic thanks to developments in the U.S.: optimism grew that American lawmakers were close to resolving the federal budget impasse. Hopes that the U.S. government shutdown was nearing an end lifted risk sentiment in early trading, which tends to favor risk-sensitive currencies like the Pound. Additionally, the Dollar’s softness (driven by those Fed rate-cut expectations and downbeat U.S. data) in the morning allowed GBP/USD to climb. However, as the day wore on, sentiment shifted. The U.S. Dollar regained some footing ahead of a crucial House vote on the funding bill – traders likely squared positions, lending support to the greenback and undermining GBP/USD’s rally. Moreover, comments from Bank of England officials remained measured, doing little to dispel the dovish cloud hanging over the Pound. By afternoon, without fresh positive news, sterling bulls lost confidence. In sum, the fundamentals for GBP/USD on Wednesday were neutral-to-bearish: early risk-on optimism and Dollar weakness gave way to renewed caution surrounding the UK’s outlook and a modest USD rebound. Traders also kept one eye on upcoming UK economic releases – including a GDP report due later in the week – which added to the hesitation to drive GBP/USD beyond its range.

USD/CAD

Technical Analysis

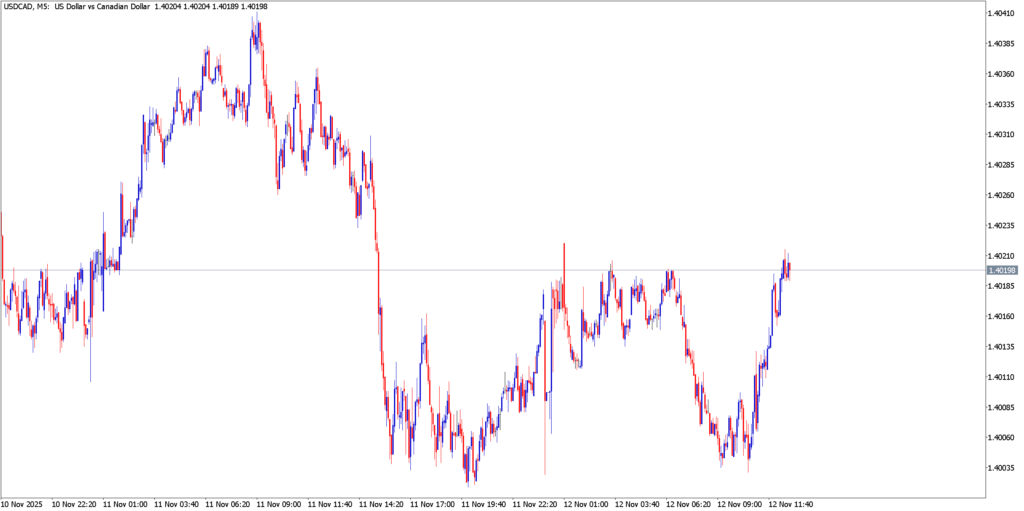

USD/CAD traded in a steady range on Wednesday, with price action largely orbiting the psychologically important 1.4000 level. In the early session, the pair actually pulled back from recent highs – sellers drove the price down through minor support at 1.4050, triggering a dip into the upper 1.3900s. On the 5-minute chart, this move marked a brief downside breakout, but follow-through was limited. After touching an intraday low in the 1.3980s, USD/CAD quickly found support and bounced back above 1.4000. The subsequent hours saw the pair stabilize within a tight band, roughly between 1.3990 and 1.4030. This created a visible base just under 1.4000 – each time the rate slipped toward that area, buying interest emerged to prop it up. Conversely, rallies stalled near 1.4040–50, where intraday resistance formed after the morning decline. The net result was a flattened trajectory through the European and New York sessions, as neither bulls nor bears managed a decisive push. Technical indicators reflected this equilibrium: short-term moving averages flattened and converged, while volatility measures on the M5 timeframe eased. Notably, USD/CAD’s ability to hold above its prior support (1.3980) suggested underlying bid strength, even as momentum to the upside waned. By the close of play, the pair was essentially unchanged, forming a cautious holding pattern around 1.4000 that traders will be watching for a breakout in the coming days.

Fundamental Analysis

Wednesday’s quiet USD/CAD performance belied a backdrop of offsetting fundamental forces. On the Canadian side, there were no major data releases during the session, leaving the Loonie without a fresh domestic catalyst. However, recent context kept traders attentive. The Bank of Canada’s late-October rate cut (a 25 bps reduction on Oct 29) still loomed in the background, generally a weight on the Canadian Dollar. Yet, that dovish policy move was partly counterbalanced by Canada’s strong jobs report from the prior week, which showed the labor market holding up better than expected. This mixed outlook meant the CAD didn’t have a clear one-way driver. Meanwhile, commodity prices – a key pillar for the Loonie – were mildly supportive. Crude oil traded near the $60 per barrel mark, historically a constructive level for the oil-linked Canadian currency. That said, oil prices remained range-bound and failed to break higher, so any positive influence on CAD was limited. On the U.S. side of the equation, the Greenback’s trajectory was also muddled. Early in the day, the Dollar was still digesting the implications of a potential government shutdown resolution. News that U.S. lawmakers were advancing a deal to fund federal agencies improved broad market sentiment (a slight negative for the safe-haven USD), but at the same time, the prospect of political clarity removed an element of risk, preventing any aggressive sell-off in the Dollar. Additionally, U.S. bond yields and the Fed outlook remained relatively steady midweek – traders recognized that while the Fed is inclined to ease in coming months, there was no new information on Wednesday to jolt expectations. The upshot was a fundamental stalemate: the USD remained firm enough (with the Dollar Index hovering just below the 100 level) to keep USD/CAD supported, while the CAD had just enough going for it (okay domestic fundamentals and stable oil) to fend off a larger USD/CAD rally. This balance was perfectly reflected in the pair’s flat closing tone. Investors appear to be biding time on USD/CAD, awaiting a clearer signal from either a swing in global risk appetite or the next big North American economic data release.

Market Outlook

Wednesday’s forex session ended without dramatic breakouts, but it set the stage for potential moves ahead. Overall market sentiment was cautiously optimistic – the prospect of an end to the U.S. government shutdown removed a major cloud of uncertainty, yet traders remained measured in their positioning. The US Dollar’s wavering performance against the Euro, Pound, and Canadian Dollar highlights a broader theme: shifting expectations on U.S. monetary policy and politics are guiding currency flows, though no single narrative dominated midweek.

Going forward, traders will be closely watching whether these major pairs can push beyond the technical levels that held firm on the 12th. For EUR/USD, the 1.1600 barrier stands out – a clear move above it, especially if reinforced by soft US economic data or dovish Fed speak, could open the door to further euro gains. Conversely, a break below recent support around the mid-1.1500s might signal a deeper correction if the Dollar finds renewed strength. In GBP/USD, the focus shifts to whether the Pound can regain momentum despite domestic headwinds.

Any upside surprise in UK data (such as an upbeat GDP reading or inflation uptick) could revive sterling and challenge the 1.3200 region, while continued weak economic signals might see 1.3000 tested again, particularly if global risk sentiment sours. USD/CAD traders will monitor the 1.4000 pivot – sustained trade below that level might indicate growing confidence in the Loonie (perhaps driven by rising oil prices or hawkish tilt from the BoC), whereas a climb above 1.4100 would underscore Dollar resilience. Broadly, market participants are entering the latter part of the week with a vigilant eye on upcoming catalysts: U.S. inflation data and Fed commentary, European growth indicators, and commodity price swings will all help determine if the Dollar’s midweek wobble turns into a larger trend. As the dust settles on the political drama in Washington, attention will shift back to core economics. Traders should be prepared for potential volatility if any of these awaited events deliver a surprise. In the meantime, the prevailing mood is one of guarded optimism tempered by prudent caution – a tone likely to carry into the next sessions unless jolted by new developments.