Monday’s session did not deliver a clean directional break, but it did show the market reaching a crucial decision point. Reuters reported that the dollar was broadly steady as traders balanced two competing narratives: renewed fear around escalation in the Iran war, including Trump’s deadline for the Strait of Hormuz to reopen, and emerging speculation that some form of ceasefire diplomacy might still be possible. Brent crude stayed above $109, inflation fears remained embedded, and the dollar retained the haven support it had built through late March. But unlike the more one-way flows seen earlier in the conflict, Apr. 6 felt more like a market waiting to decide whether the war premium was still justified at full strength.

That nuance matters because the dollar was no longer rising on fresh panic alone. It was being held up by the residual logic of the previous month: higher oil, tighter global financial conditions, reduced confidence in cuts, and the sense that the U.S. economy remained less directly exposed than Europe, Japan, or the UK to the energy shock. Yet the fact that Reuters framed the session around both escalation fears and ceasefire hopes showed that investors were beginning to test whether the greenback’s risk premium had become overextended.

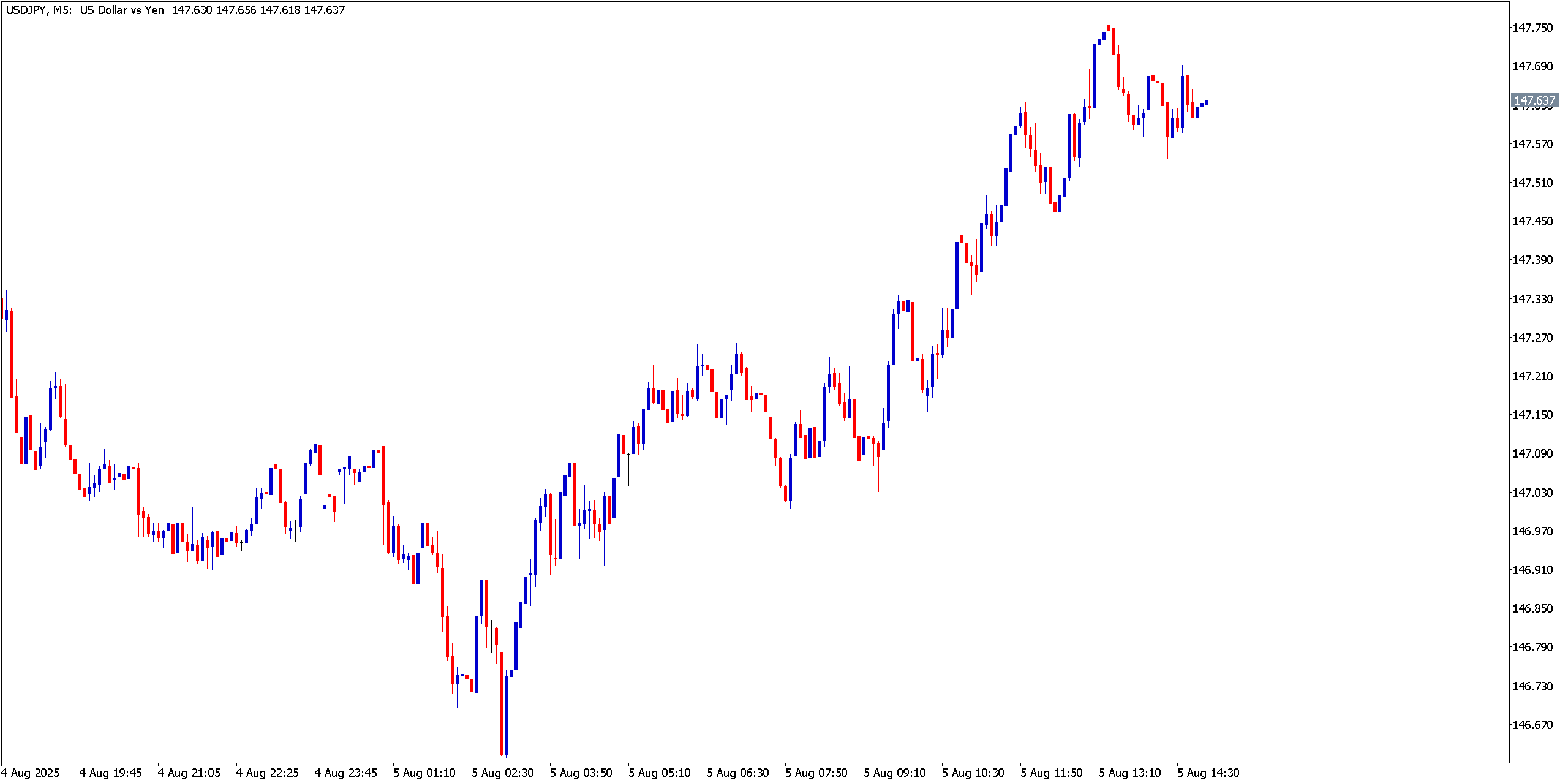

USD/JPY

Technical Analysis

USD/JPY was the most important pair on Monday because it was trading right at the point where macro strength met political discomfort. Reuters reported the yen was flirting with the crucial 160-per-dollar area, and that alone tells you what the technical structure looked like: not a normal trend continuation, but an advance entering increasingly intervention-sensitive territory. When a pair moves into a zone where authorities have previously acted, chart levels stop behaving like purely technical levels and start behaving like policy tripwires. That gives the pair a strange combination of momentum and fragility. It can remain supported, but each new push higher becomes less stable and more reactive to headlines.

Fundamental Analysis

The yen was under pressure for reasons that went well beyond generic dollar strength. Reuters reported that the Bank of Japan warned the Middle East conflict could worsen regional economic conditions, highlighting higher import costs and supply chain strain. That is especially important for Japan because the country remains heavily exposed to imported energy, so a war-driven oil shock is directly negative for the yen even before broader rate differentials enter the picture. At the same time, Reuters said a 70% probability of a BOJ hike remained priced in for the late-April meeting, but conflict uncertainty was intensifying debate over whether policymakers could move. This is precisely why USD/JPY remained elevated: Japan’s inflation pressure was worsening, but not in a way that automatically strengthened the currency. Instead, it complicated the BOJ’s decision-making while leaving the dollar with both haven support and relative yield support.

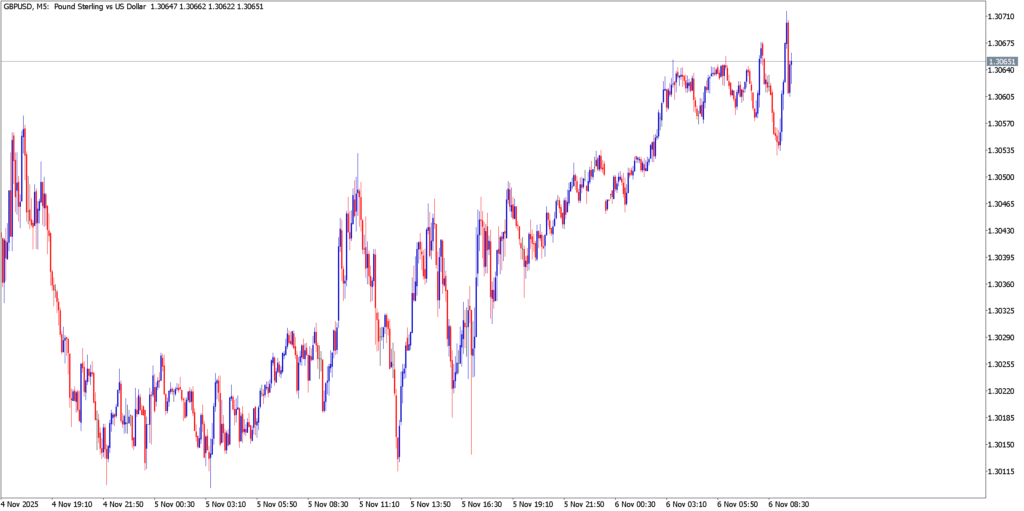

GBP/USD

Technical Analysis

GBP/USD was not the week’s most explosive pair on Monday, but it was instructive because it refused to regain strong upside traction even when the dollar stopped rising outright. The pair behaved like a market trying to base, but not one attracting real conviction. In practical technical terms, that means short-term stabilization without an actual turn in structure. Those are often the weakest kinds of rebounds, because they depend entirely on the other side of the pair easing rather than on fresh buying interest in the base currency.

Fundamental Analysis

Reuters’ sterling coverage from Apr. 7 described the pound as edging higher but still sitting near a more than four-month low against the dollar, while highlighting the UK’s exposure to energy imports and fragile public finances. That retroactively fits Monday’s action very well. Sterling was able to stop falling, but it still carried meaningful structural baggage: the UK had not escaped the inflation consequences of the oil shock, and the market remained uneasy about the interaction between higher costs, weak growth, and fiscal constraints. So GBP/USD on Apr. 6 was not really a “buy sterling” trade. It was more accurately a “pause the dollar rally until the next headline” trade.

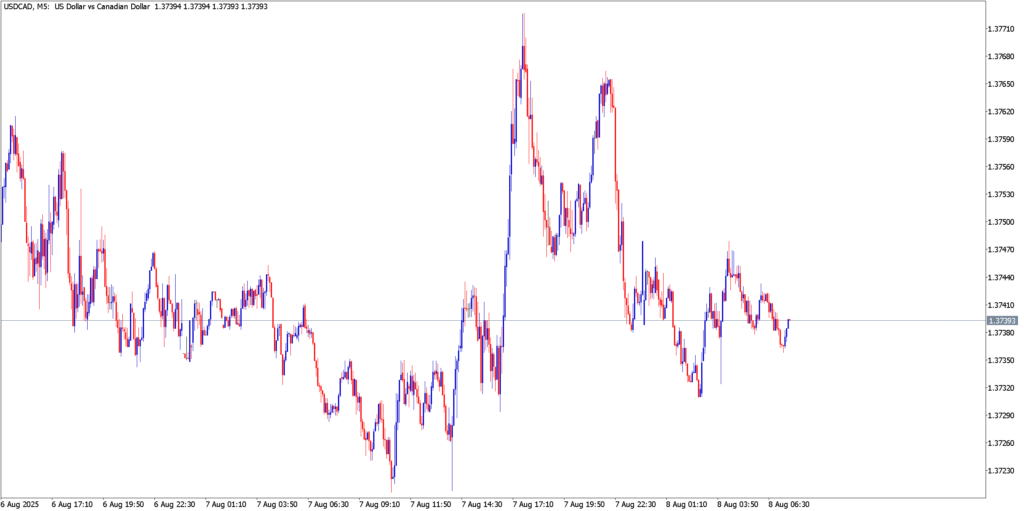

USD/CAD

Technical Analysis

USD/CAD stayed firm, which was telling because the pair might normally have struggled more with oil elevated. Instead, it behaved like a pair whose primary driver remained broad dollar preference rather than crude alone. That left the technical profile tilted upward but not euphoric: more of a grind than a breakout. In macro-driven weeks, that kind of price action often turns out to be more durable than the noisier moves because it reflects steady institutional positioning rather than emotional flow.

Fundamental Analysis

Reuters reported on Apr. 6 that Canada’s services sector had contracted for a fifth consecutive month, while the loonie posted only limited gains. That combination mattered. Even though Canada can benefit from higher oil in many environments, domestic weakness and ongoing geopolitical stress prevented CAD from fully monetizing the commodity move. Reuters also noted that risk premiums were still elevated and that the U.S. dollar remained overvalued because markets were still embedding geopolitical risk. So USD/CAD remained supported not because Canada had no oil tailwind, but because that tailwind was still weaker than the market’s desire to own dollars until the conflict picture clarified.

Market Outlook

By the close, Apr. 6 had clarified that the dollar still held the strategic advantage, but that traders were starting to test the limits of the war premium. USD/JPY remained the most politically sensitive pair, GBP/USD remained too weak to lead a genuine anti-dollar move, and USD/CAD showed that even commodity support could not yet fully dislodge broad dollar preference. The market was clearly waiting for a headline catalyst large enough to validate or unwind the entire late-March/early-April macro regime.

Check out our other forex market analysis: