Tuesday’s forex session was defined by political breakthroughs and divergent economic signals. The U.S. Dollar caught a bid across the board as Washington appeared close to ending its longest-ever government shutdown, boosting market sentiment. At the same time, weak UK labor data sent the British pound tumbling, while an uptick in European investor confidence struggled to buoy the euro against the greenback. With North American markets thinned by the Veterans Day holiday, major currency pairs saw technical ranges tested on lower liquidity. Overall, the day’s theme was one of dollar resilience – fueled by U.S. fiscal relief and growing Fed rate-cut chatter – set against a backdrop of soft UK fundamentals and cautious optimism in Europe. In this recap, we break down the EUR/USD, GBP/USD, and USD/CAD price action on the 5-minute charts, coupled with the key technical levels and fundamental drivers from November 11, 2025.

EUR/USD

Technical Analysis

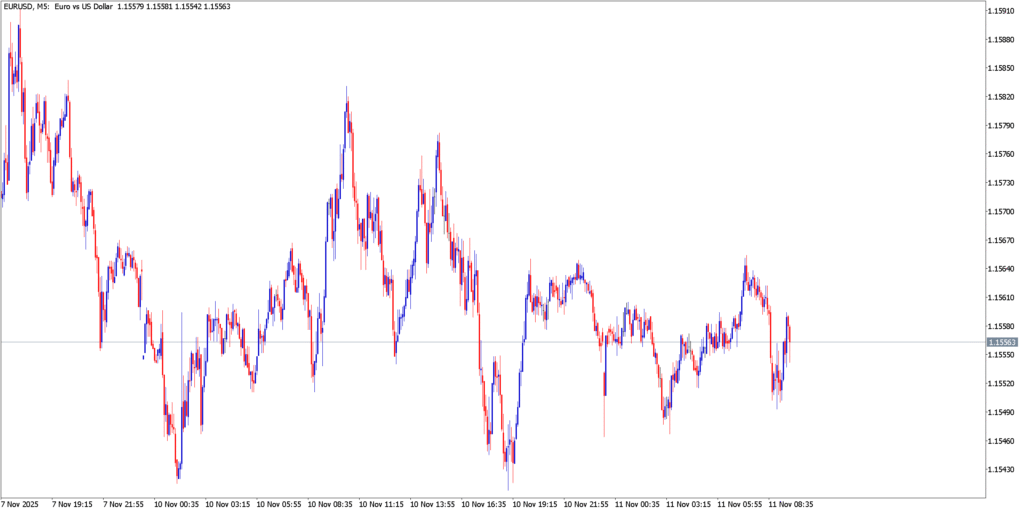

On the 5-minute EUR/USD chart, price action was largely range-bound as traders digested mixed cues. The pair spent the session oscillating roughly between $1.1530 support and $1.1570 resistance, failing to sustain any breakout. Early in the day, euro-dollar attempted a modest rise, but bullish momentum faded near the 1.1560s – around the prior session’s peak. A lack of follow-through above 1.1570 signaled persistent overhead supply. Conversely, dips toward the mid-1.15s found buyers. Notably, support around $1.1535 (just above the day’s low) held firm, aligning with minor demand seen on the chart. The 5-minute candlesticks show no dramatic spikes, reflecting the subdued volatility. By the U.S. afternoon (when liquidity was lower due to the holiday), EUR/USD was drifting near $1.1550, essentially unchanged from its European open. Technical indicators suggested a neutral intraday bias – with short-term moving averages flattening out – as neither bulls nor bears seized control. In summary, EUR/USD’s trend was flat on the session, respecting its established range amid an absence of a decisive catalyst.

Fundamental Analysis

Fundamental developments provided a push-and-pull dynamic for the euro. On one hand, sentiment toward the U.S. dollar improved markedly thanks to optimism that the U.S. government shutdown would soon end. News broke that President Donald Trump endorsed a bipartisan deal to fund the government and end the prolonged shutdown. This lifted the dollar broadly, as an imminent reopening was seen as bolstering U.S. economic confidence and potentially averting further consumer sentiment damage. Indeed, analysts noted that the agreement to resume federal operations “eases fears of a prolonged hit to household confidence” in the U.S.. This political breakthrough limited the euro’s upside against the greenback.

On the other hand, the euro saw only a modest tailwind from European data. Germany’s closely watched ZEW Economic Sentiment survey for November came in slightly better than expected, rising to about 41 (index points) compared to October’s 39 reading. A higher ZEW index indicates improving optimism among financial analysts, which under normal circumstances would be euro-supportive. However, the positive surprise was relatively muted in impact – likely because the result still pointed to only cautious optimism and because traders were more fixated on U.S. developments. Furthermore, the Eurozone’s economic outlook remains clouded by weakness in consumer demand (recent Eurozone Sentix investor confidence fell to -7.4, a sign of deteriorating sentiment). European Central Bank officials struck a steady tone as well: Vice President Luis de Guindos reiterated that current ECB policy is “appropriate” with inflation nearing target, suggesting no imminent easing to juice growth. With no major Eurozone surprises and U.S. news dominating, EUR/USD’s fundamental backdrop on the day favored consolidation. The pair’s inability to rally on decent German data underscored the dollar’s support from the U.S. shutdown news. Traders also kept one eye on central banks – the Fed’s evolving stance versus the ECB’s hold – which continued to lend the euro some underlying support via narrowing policy divergence, even as short-term news favored the dollar. All told, EUR/USD ended the day little changed, as modest Eurozone optimism was offset by a firm U.S. dollar tone.

GBP/USD

Technical Analysis

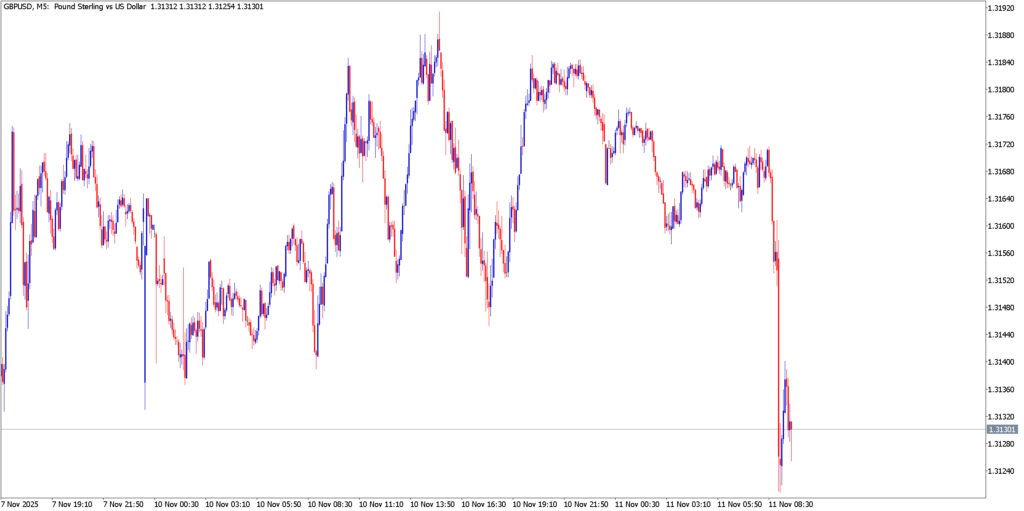

GBP/USD had an event-driven tumble on the 5-minute chart, as UK data releases sparked a selloff in the London morning. The pair began the session near $1.3160, but swiftly fell below $1.3120 once the disappointing jobs numbers hit the wires. A sharp bearish candle around 9:00 GMT marks the moment the pound broke below its intraday support, reflecting a surge of selling volume. In the aftermath, GBP/USD extended its decline toward the $1.3100 handle, making a session low in the 1.3090s before finding a foothold. This intraday low coincided with a minor support area from the previous day’s price action, where buyers tentatively stepped in. However, any rebound attempts were feeble. The 5-minute RSI and stochastic indicators turned decisively south after the data drop, and remained in bearish territory for several hours. Despite a gentle bounce off the lows by early New York trading, the pair struggled to regain 1.3140 – a level that had acted as support pre-data and now served as interim resistance. By day’s end, GBP/USD hovered around 1.3120, nursing a loss. The technical picture thus showed a clear downward intraday trend with lower highs and lower lows. The pound’s failure to recover much of its losses signaled weak momentum, as traders absorbed the poor UK fundamentals. Key short-term resistance formed at $1.3140–50, while support around $1.3100 remained vulnerable if bearish pressure were to continue. In summary, GBP/USD spent the day on the back foot, with the charts depicting a decisive bearish reaction and only a partial late-day stabilization.

Fundamental Analysis

Sterling’s slide was driven by an unfavorable batch of UK economic data, which heightened concerns about the British economy and future Bank of England policy. The UK labor market report for October was notably weak. Britain’s unemployment rate jumped to 5.0%, the highest in four years, exceeding forecasts of 4.9%. This uptick in joblessness – coming sooner and faster than many anticipated – underscored a worsening jobs market as the country heads into winter. At the same time, wage growth showed signs of cooling. Excluding bonuses, average earnings rose 4.6% in the July–September period, slightly slower than the previous 4.7% pace, according to the Office for National Statistics. The data “bolstered expectations for a Bank of England interest rate cut next month”, as easing pay pressures and rising unemployment give the BoE more room to stimulate without stoking inflation. In fact, the BoE had just held rates at 4.0% last week and hinted that rate reductions could come as soon as December. Tuesday’s figures appeared to validate that dovish bias. Not surprisingly, the British pound dropped about a quarter of a cent against the dollar after the data release. Traders reacted to the prospect that lower rates and a softer economy would erode the pound’s yield appeal and growth outlook.

Compounding the pound’s troubles, the broad USD strength tied to the U.S. shutdown deal optimism added another headwind. With the dollar in demand, GBP/USD faced a two-pronged fundamental drag (weak UK data and a firmer USD). There was little in the way of positive UK news to counteract these forces. BoE policymakers have emphasized they need to see sustained easing in inflationary pressures before cutting rates, and Tuesday’s jobs report, showing slack building in the labor market, met that criteria. Political factors were relatively quiet in the UK (Brexit was not a front-burner issue on the day), so the focus remained squarely on economics. In summary, GBP/USD’s fundamental bias turned bearish on November 11 as the UK’s economic momentum appeared to falter. The pound’s decline was an intuitive response – weaker growth and sooner rate cuts are a classic recipe for currency depreciation. Unless upcoming UK data (like the GDP report due later in the week) surprises to the upside, sentiment toward sterling may stay subdued in the near term.

USD/CAD

Technical Analysis

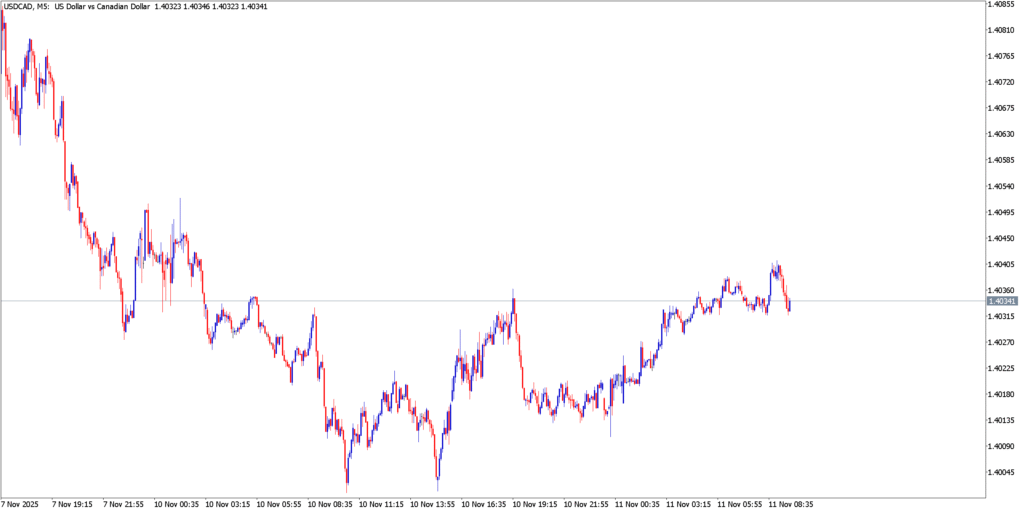

USD/CAD started the day in recovery mode on the 5-minute chart, rebounding after two prior sessions of declines. In Asian trading hours, the pair found a floor around C$1.4000, which had proven to be a firm support level. From this psychological support, USD/CAD climbed steadily, forming a series of higher lows through the European session. The technical bounce was evident as the pair pushed up to around 1.4050 by mid-morning – a level that roughly coincided with the 50% Fibonacci retracement of its drop since late last week. The short-term moving averages on the 5-minute timeframe flipped to a bullish alignment as the day progressed, reflecting the shift in intraday momentum toward the upside. Around 1.4050–1.4060, the advance paused, suggesting this area served as immediate resistance. Indeed, the price struggled to break above C$1.4060, which corresponded to the highs from Monday’s session. A minor double-top pattern may have formed near that peak on the intraday chart, leading to some consolidation in the early U.S. hours. Given the U.S. and Canadian bank holiday, trading volumes were lighter, and USD/CAD mostly drifted sideways in a tight band (roughly 1.4025–1.4055) into the afternoon. By the close of Tuesday’s session, the pair held around C$1.4040, preserving most of its intraday gains. Technical signs point to near-term bullish bias – the successful defense of 1.4000 support and the intraday uptrend – but also highlight overhead resistance just above 1.4050. A clear break beyond C$1.4060 could open the door to retest the recent highs (~1.4100), whereas a slip back below C$1.4000 would negate the current rebound. In summary, USD/CAD’s 5-minute chart showed a constructive recovery, albeit within its broader range, as the pair rebounded off key support and stabilized into day’s end.

Fundamental Analysis

In fundamental terms, USD/CAD’s movements reflected a tug-of-war between U.S. dollar strength and the Canadian dollar’s own supportive factors. The early gains in USD/CAD were driven largely by the U.S. side of the equation. With President Trump and Senate leaders making tangible progress toward ending the budget impasse in Washington, the U.S. dollar found fresh backing. Traders reasoned that resolving the shutdown – which had stretched on for weeks – would remove a downside risk for the U.S. economy, potentially keep U.S. Treasury yields supported, and improve overall risk appetite. Indeed, one immediate market reaction was a stronger USD across many FX pairs, including USD/CAD. Additionally, comments from Federal Reserve officials injected a dovish tint that, somewhat paradoxically, supported the dollar via improved sentiment. Fed Governor Stephen Miran suggested on Monday that staying on course with rate cuts was appropriate, even floating the idea of a 50 basis point cut in December if inflation remained subdued. Normally, the prospect of Fed rate cuts would weaken the dollar, but in this context it may have reassured investors that the Fed stands ready to bolster growth as needed – a stance that, combined with the fiscal resolution, made traders less fearful and kept the dollar in demand as a safe-haven turned yield play.

Meanwhile, the Canadian dollar (loonie) had factors working in its favor, which helped limit USD/CAD’s upside beyond the mid-1.40s. Canada’s domestic data of late has been surprisingly robust. Notably, the October Canadian employment report, released the previous week, showed a 66.6K increase in jobs (above the ~60K expected) and a dip in the unemployment rate to 6.9% from 7.1%. This strength in Canada’s labor market, coupled with an uptick in participation, has led markets to speculate that the Bank of Canada might pause its easing cycle for now. (The BoC had been cutting rates earlier in the year as inflation cooled, but better growth and jobs data reduce the urgency for further cuts.) The loonie typically draws support from such expectations of relatively higher Canadian rates. Furthermore, oil prices – a crucial driver for the petro-linked CAD – held relatively stable on Tuesday (no sharp moves were noted, as global crude traded in a narrow range), providing no additional drag on the currency. With U.S. banks closed for Veterans Day and Canadian banks for Remembrance Day, there were no new economic releases in either country on Tuesday, keeping the focus on prevailing trends. The result was a fundamentally mixed picture for USD/CAD: the U.S. dollar’s political boost pushed the pair up, but the loonie’s solid fundamentals and holiday-calmed trading curbed any runaway rally. Going forward, traders will watch if the end of the U.S. shutdown is fully priced in and whether Canadian data can continue to outperform – both will influence if USD/CAD extends this rebound or retreats back under C$1.40.

Market Outlook

Looking ahead, forex traders are turning their attention to looming economic events and whether the dollar’s newfound strength can be sustained. The resolution of the U.S. government shutdown – expected to be finalized in coming days – removes a key uncertainty and could keep the USD supported in the near term, especially if U.S. economic data remain solid. However, the focus will quickly shift to the inflation outlook and central bank responses. U.S. CPI data for October is due on Thursday, Nov 13, and a soft inflation reading could rekindle expectations for aggressive Fed rate cuts, potentially tempering the dollar’s rally. On the flip side, any upside inflation surprise would challenge the Fed’s dovish signals and might further boost the greenback. Across the Atlantic, the euro will take cues from Eurozone growth signals and ECB speak – President Christine Lagarde’s comments and any shifts in sentiment surveys will be watched after the mixed signals this week. For the pound, the trajectory will depend on whether the UK economy can show signs of life beyond the labor market slump. UK GDP figures (Q3 preliminary) are slated for later this week, and a stronger-than-expected growth print could help stem GBP’s decline by reducing fears of an imminent recession (and thus a less aggressive BoE easing path). Conversely, more weak UK data would reinforce the bearish case for sterling going into the Bank of England’s December meeting.

In the commodity currency realm, the Canadian dollar’s resilience will be tested by external factors like commodity prices and global risk sentiment. If oil prices rally or if the Bank of Canada strikes a confident tone given recent data, the loonie could outperform, capping USD/CAD. However, any resurgence of risk aversion globally – for instance, from geopolitical tensions or equity market wobbles – might play to the USD’s safe-haven strengths once more.

In summary, the forex market enters the mid-week with the U.S. dollar on solid footing, the euro in a wait-and-see mode, and the pound on its back foot. The themes of fiscal resolution and divergent monetary policy will continue to drive volatility. Traders will be positioning for the next big catalysts, with an eye on whether the dollar’s advance can weather upcoming data. As Tuesday’s action showed, shifting fundamentals can rapidly alter currency trends. The market will now seek confirmation: Will U.S. policymakers follow through on the shutdown deal and will economic releases validate the central banks’ current stance? The answers to those questions will set the tone as we move toward the end of the week. For now, dollar bulls have the upper hand, but the ever-evolving economic outlook means forex participants remain on their toes for the next twist in the tale.