Global markets are on edge mid-week as trade war tensions and central bank shifts dominate sentiment. Traders are contending with revived tariff battles under the new U.S. administration and anticipation of dovish pivots from major central banks. The IMF’s latest outlook notes that while growth forecasts have ticked upward, downside risks from higher tariffs, elevated uncertainty, and geopolitical tensions persist. Safe-haven demand is intermittently creeping in, keeping the USD and JPY supported during risk-off waves, even as investors brace for potential rate cuts. Against this backdrop, we examine GBP/USD, USD/CAD, and USD/JPY for today, factoring in technical setups from the provided charts, key price levels, and looming news events. Expect a cautious tone as traders position ahead of high-impact events – notably tomorrow’s Bank of England meeting – and react to ongoing macro-political headlines.

GBP/USD

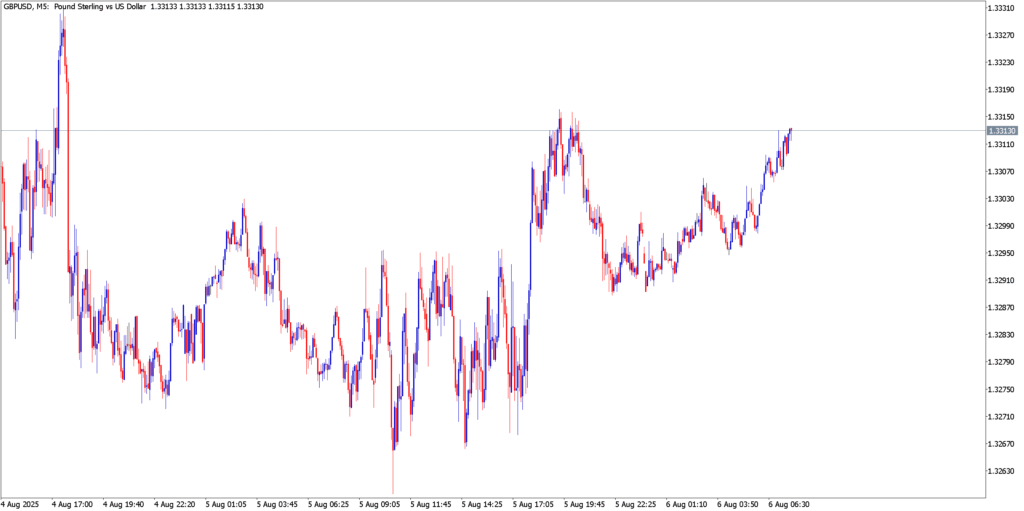

GBP/USD’s 5-minute chart shows the pair attempting to claw back losses, bouncing off support near $1.3260 and revisiting the $1.3300 handle. After a steep slide in July, sterling found an intermediate low around $1.3140 last week, and the recent bounce has brought it back into a tight range ahead of the Bank of England decision. Price is forming small-bodied candles (even a doji on the daily chart) as bulls lack conviction at $1.33 – a psychological level aligning with the 50-period moving average on the 4H chart. Immediate **resistance stands at $1.3325–1.3340, just above current pricing, and a break higher could open the door to the key $1.3400 pivot area. On the downside, support from the recent rebound lies at $1.3260 (the week’s floor) with stronger support around $1.3180–1.3140 (last week’s lows). The short-term trend has turned into a base-building phase – a relief from the prior downtrend – but the pound’s upside appears capped unless a fresh catalyst emerges.

Fundamentals

The pound’s fate today hinges on central bank expectations and economic signals. Market chatter is centered on the Bank of England’s meeting tomorrow, where policymakers are widely expected to cut rates by 25 bps amid signs of cooling inflation and growth risks. In fact, the BoE has already begun an “insurance” rate-cut cycle, trimming the Bank Rate from 5.25% earlier this year to the current 4.25%. With persistently high UK inflation slowly easing, the BoE is striking a cautiously dovish stance, and futures imply a 96% chance of a cut at this meeting. This looming policy easing has tempered GBP’s recovery – any dovish surprise or gloomy forecasts in the BoE’s Monetary Policy Report (due alongside the decision) could send GBP/USD back down through support. On the U.S. side, the dollar has been on the back foot since last Friday’s disappointing Non-Farm Payrolls, which undercut the Greenback’s recent strength and bolstered bets that the Fed’s next move is a rate cut. Yesterday’s ISM Services PMI miss (50.1 vs ~51.5 expected) further underscores a slowing US economy, reinforcing Fed dovish expectations. For today, with no major UK data, traders will eye any Fed speakers (Collins, Cook, Daly are on the docket) for hints on September’s FOMC plans.

Trade idea

The bias on GBP/USD is neutral-to-bearish going into the BoE. A sell-on-rallies approach could be considered – for instance, fading any spikes toward $1.3340–50 resistance with a stop above $1.3400, targeting a pullback to the $1.3260 area. Conversely, if a hawkish BoE surprise or USD weakness drives a clear break above $1.3350, bulls might aim for a quick run toward the $1.3400–1.3450 zone – though caution is warranted with event risk so near. Overall, sterling traders appear to be in wait-and-see mode, with tight ranges likely persisting until tomorrow’s BoE fireworks.

USD/CAD

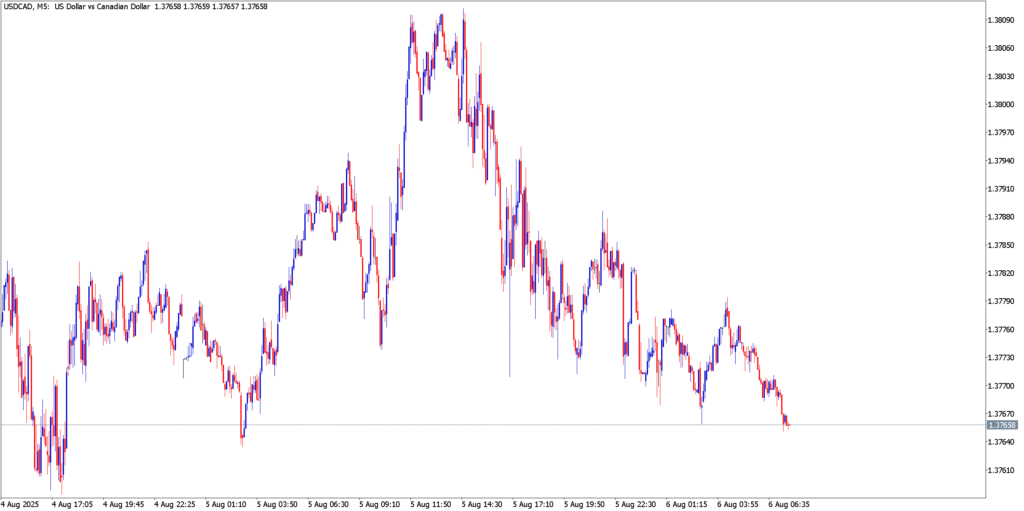

USD/CAD’s chart (5-minute) illustrates a consolidative pause just under the 1.3800 mark, as the pair digests its recent upswing. After five consecutive days of gains into end-July, USD/CAD touched the high-1.38s early this week before momentum stalled. The 1.3800 level has acted as a psychological barrier, with bulls unable to secure a daily close above it. We see a modest pullback from the 1.3810 area (the recent swing high) down to the 1.3750–1.3760 support zone in overnight trading. This area aligns with the 5-minute chart’s visible lows and has so far contained the dip. Short-term bias remains mildly bullish – the pair is still posting higher lows, and a potential bullish flag pattern may be forming just below resistance. Key resistance is evident at 1.3800–1.3820 (recent highs); a decisive break there would expose the next upside targets around 1.3900, a zone of strong resistance highlighted by prior highs. On the flip side, if 1.3750 support gives way, the next support levels to watch are around 1.3700–1.3720, and below that the 1.3585 region (bullish invalidation on a daily closing basis). Technical indicators (e.g. RSI) on higher timeframes remain in bullish territory after breaking out from neutral, suggesting buy-on-dips mentality could persist unless a catalyst reverses the trend.

Fundamentals

The Canadian dollar (CAD) is struggling to find footing as commodity dynamics and central bank expectations tug it in opposite directions. On one hand, crude oil’s weakness is a clear headwind: WTI oil is languishing in the mid-$60s, pressured by rising OPEC+ supply and worries of softer global demand. OPEC+ surprised markets by agreeing to boost output by 547k barrels/day in September, stoking fears of a supply glut. With Canada being a major oil exporter, the slump in oil prices directly undermines the Loonie, as lower crude tends to have a negative impact on CAD’s value. This has helped keep USD/CAD buoyant on dips. Additionally, Canada’s latest data showed a widening trade deficit (June shortfall C$5.86B vs C$5.8B expected), reflecting weaker exports – partly due to U.S. tariffs hitting sectors like softwood lumber. (Notably, Canadian PM Mark Carney announced support measures for lumber exporters this week, amid tariff-related struggles.) On the other hand, the U.S. dollar’s upside is being checked by growing odds of Fed rate cuts. Markets are now pricing in 80–90% probability of a Fed rate cut in September after a string of softer U.S. data. Yesterday’s ISM services dip to 50.1 – barely expansionary – and prior weak jobs numbers have fueled speculation that the Fed will “blink” and ease policy soon. This dynamic caps USD/CAD’s rallies, as traders balance higher U.S.-Canada rate differentials (Fed still holds ~5% vs BoC at 2.75%) with the prospect of those differentials shrinking quickly if the Fed eases.

Trade idea

The path of least resistance in USD/CAD appears upward, but it’s a grind. A potential setup is to buy on dips near support – e.g. accumulate around $1.3720–1.3750, in anticipation of a break above $1.3800. Stops could be placed under $1.3700 (just below the recent consolidation floor), with initial targets at $1.3900 and $1.4000 (major resistance area). This trade leans on the idea that weak oil and global trade concerns continue to pressure CAD. However, one should stay nimble: any sharp rebound in oil prices (perhaps from a bullish EIA inventory report or geopolitical flare-up) or hawkish surprise from Fed speakers could strengthen CAD and send USD/CAD lower. In that case, a break below $1.3720 would signal momentum shifting – nimble traders might then flip bias and look for a drop toward the 1.3600s. For now, though, the bias is mildly bullish on USD/CAD, with the pair retaining a buy-the-dip character amid trade jitters and commodity softness.

USD/JPY

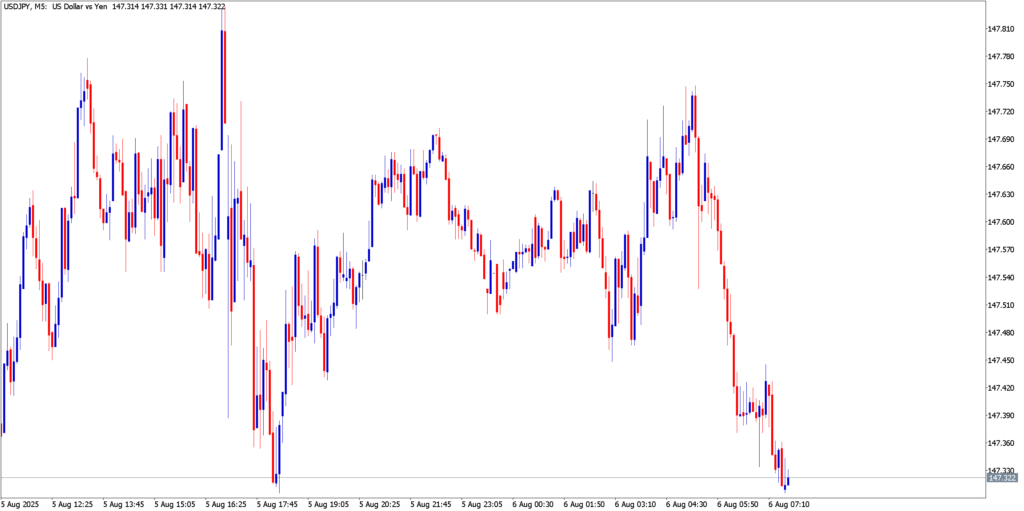

USD/JPY’s 5-minute chart reveals choppy action as the pair oscillates in the mid-147s, constrained below recent highs. After an initial surge, dollar-yen failed to clear the ¥147.80 resistance (a level that aligns with late-July swing highs) and has since eased back toward ¥147.30. The short-term trend is lackluster – rallies are struggling to sustain, evidenced by lower highs on the intraday chart after each push toward ¥147.8. Key resistance overhead lies at ¥147.80–148.00; this zone halted the advance yesterday and marks the ceiling of the week’s range. Beyond that, ¥148.50 and ¥149.00 loom as further resistance, but market participants are acutely aware that any move toward ¥150.00 could trigger official alarm. On the support side, minor support is seen around ¥147.00–147.20 (where the dollar found bids earlier in the week). Below there, the ¥146.60–146.80 region is noteworthy – it corresponds to previous breakout levels and was cited as support in technical analyses. A drop under ¥146.60 would indicate a short-term trend reversal to the downside, potentially exposing ¥145.00–145.50 next. For now, however, the pair remains range-bound, reflecting a tug-of-war between USD strength and JPY safe-haven demand.

Fundamentals

Policy divergence and risk sentiment are the twin drivers for USD/JPY. Earlier in the week, the Bank of Japan’s meeting minutes and communication struck a mixed tone – on one hand slightly dovish (most members favored holding rates in June amid downside risks), but on the other hand affirming that if inflation and growth align with forecasts, more rate hikes are on the table down the road. In fact, at last week’s policy meeting the BoJ raised its inflation forecast to 2.7% for this fiscal year and signaled openness to tighten further if needed. This has introduced a slow-burning undercurrent of hawkish expectation for Japan, but in the near term the BoJ is still in ultra-easy mode (policy rate still negative). Meanwhile, U.S. yields have been softening as Fed rate cut bets build – the US-Japan 10-year yield spread has narrowed steadily over recent months. Such narrowing yield differentials put downside fundamental pressure on USD/JPY, as the dollar’s carry advantage erodes. At the same time, global risk appetite is fragile: trade war escalations and slowdowns usually benefit the yen. However, the yen has softened in the past 24 hours after those BoJ minutes did not indicate any imminent tightening; USD/JPY popped higher yesterday to test ¥147.7. But any USD strength may be fleeting. Traders know that as USD/JPY climbs toward the ¥150.0 threshold, intervention risk grows palpable – Japan’s finance ministry has previously stepped in to stem yen free-fall around these levels. Analysts warn that around ¥155 would be an extreme pain point, but even mid-¥149s could spark verbal intervention. Thus, upside moves face political headwinds. In the immediate term, focus will be on U.S. data and yields: if we see further signs of U.S. economic weakness (and thus lower yields), USD/JPY could quickly turn south. Today’s catalysts include any fallout from tariff news (the U.S.-Japan trade agreement struck recently has removed some uncertainty, but broader U.S.-China/EU tariff moves remain a concern) and the general risk tone (equity wobble could send yen higher).

Trade idea

With the risk/reward skewing toward yen strength at these levels, one strategy is to sell USD/JPY rallies. For instance, consider shorting in the ¥147.5–148.0 zone, with a tight stop above ¥148.8 (above last week’s highs), aiming for a retracement to ¥146.50 or lower. This play banks on the idea that narrowing yield spreads and any risk-off waves will favor JPY. A more aggressive target could be the mid-¥145s if momentum builds. Alternatively, if an unexpected risk-on surge or hawkish Fed tone sends USD/JPY decisively above ¥148.8, that could invalidate the bearish bias – in that case, bulls might target the ¥150 mark, but they would do so nervously given likely official pushback. Overall, expect choppy trading in USD/JPY, with a slight bearish tilt as long as it stays below the strong ¥148–¥149 resistance zone.

Market Outlook

In summary, the forex bias for the day is cautious and slightly tilted by expectations of central bank easing. The U.S. dollar index’s recent rebound has been curtailed by growing conviction that the Fed will cut rates soon, so USD is struggling to extend gains across the board. This creates a nuanced picture: dollar-pairs may not follow the usual risk-off script uniformly. For GBP/USD, the immediate bias is neutral, flipping to bearish if the BoE delivers a dovish surprise tomorrow. Sterling’s relief rally is running on fumes ahead of the event, and traders are wary of another leg down if BoE Governor Bailey emphasizes downside risks. USD/CAD holds a mild bullish bias (USD strength) intraday, driven by weak oil prices and Canada’s trade woes, though any sign of supply tightening (or a broader market risk-on swing) could spur a CAD recovery. USD/JPY feels heavy under 148, reflecting that the yen’s safe-haven appeal and narrowing yield gap are offsetting the dollar’s yield advantage – thus we lean slightly bearish on USD/JPY unless global sentiment drastically improves. Correlated markets are also in focus: equities are subdued amid trade-war noise, and oil’s downtrend is a key factor for CAD, while Treasury yields (hovering off recent highs) are a barometer for yen crosses. For the rest of the day, traders should watch for surprises from Fed speakers, any last-minute political news (e.g. tariff announcements or negotiations), and positioning into the Asian session where we could see adjustments before the BoE meeting. Overall, a defensive trading stance is warranted – it’s a day to be nimble, respect key technical levels, and be prepared for volatility if any headlines hit. With major event risk on the horizon, capital preservation and careful trade selection will be paramount.