Friday finally brought a clear U.S. macro event back into the center of the FX conversation: the March jobs report. Reuters reported that nonfarm payrolls rose by 178,000, well above the 60,000 consensus forecast, and the unemployment rate fell to 4.3%. The market response was straightforward at first: Treasury yields rose and the dollar got support because stronger headline hiring reduced the urgency for the Fed to ease. Reuters’ instant view coverage said the report would likely keep the Fed on the sidelines.

But Friday was not a simple “strong data equals strong dollar” session. Reuters also emphasized that the report overstated labor-market health: the average workweek shortened, wage growth slowed to its weakest pace since May 2021, and the unemployment-rate decline was heavily driven by 396,000 people leaving the labor force. So the jobs report reinforced the dollar at the headline level, but the underlying detail kept the broader economic picture more complicated. That nuance mattered, especially with the Iran war still casting a shadow over inflation, supply chains, and growth expectations.

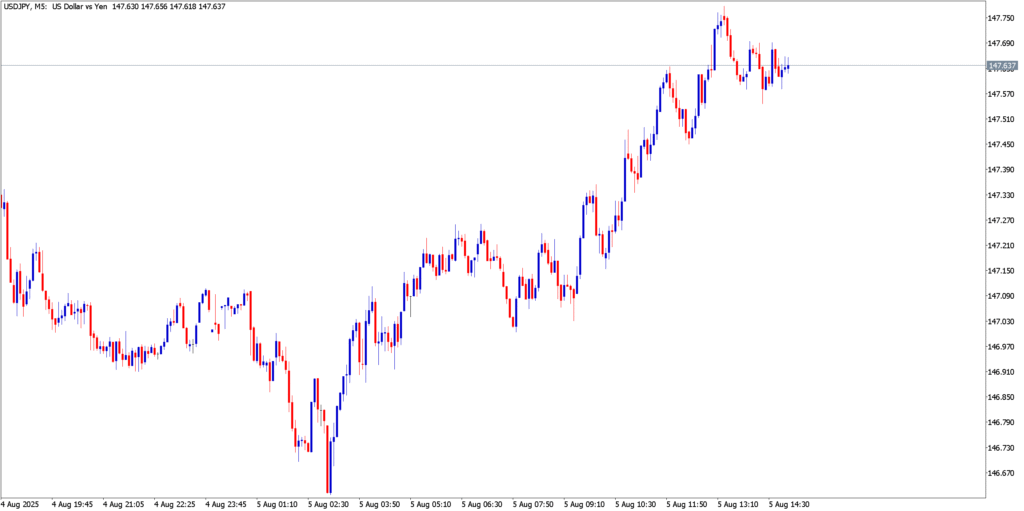

USD/JPY

Technical Analysis

USD/JPY remained one of the most important and most unstable expressions of Friday’s combined data-and-geopolitics backdrop. Strong payrolls and firmer yields naturally supported the pair, but it was still trading close to 160, where every upside extension came with higher policy risk. Technically, that creates a pair that can keep grinding upward, but with an unusually asymmetric risk profile: limited room for complacent upside, but substantial room for sharp pullbacks if officials act or even just escalate their rhetoric.

Fundamental Analysis

Reuters reported that Japanese Finance Minister Satsuki Katayama said authorities were prepared to respond fully on all fronts as exchange-rate volatility affected the public and the economy, while traders put the effective intervention danger zone in the 161–162 area unless the BOJ moved first at its late-April meeting. At the same time, Reuters’ payrolls coverage showed stronger headline hiring and higher Treasury yields. Put together, that meant USD/JPY still had macro support, but it was now leaning harder into the most politically uncomfortable part of its range.

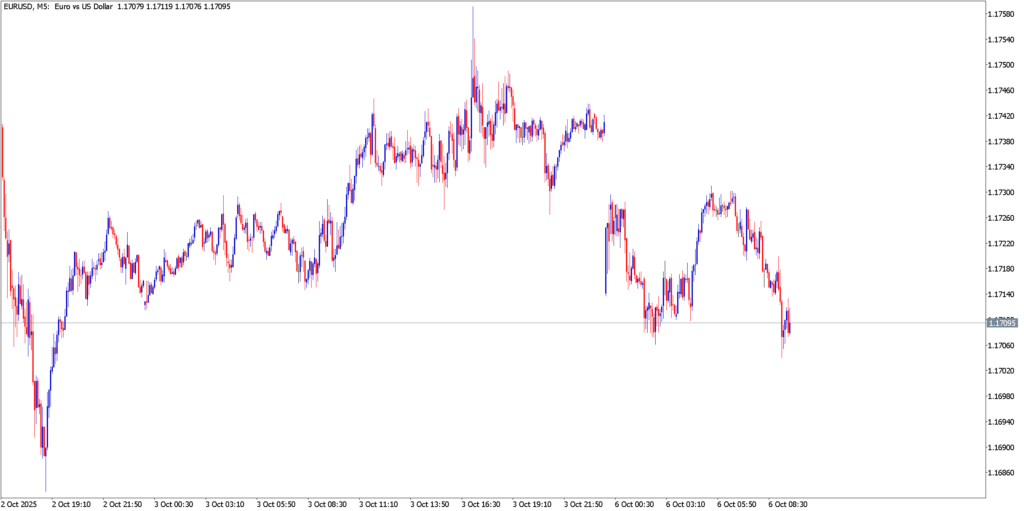

EUR/USD

Technical Analysis

EUR/USD stayed pressured and looked unable to convert earlier-week stabilization into anything more durable. Friday’s stronger U.S. payroll headline reinforced the sense that the pair remained in a broader bearish weekly structure, where any rebound required not just softer war fears but also a clear deterioration in U.S. macro momentum. That second condition did not arrive. Technically, the euro therefore remained defensive.

Fundamental Analysis

The euro’s problem on Friday was relative, not absolute. The U.S. jobs report was strong enough to keep the Fed patient, while Europe still faced the same imported-energy vulnerability that had weighed on it all week. Reuters also noted that the jobs report likely had little immediate impact on the Fed’s current rate range because the war’s supply-chain consequences still needed time to work through the economy, but the odds of a cut this year had diminished sharply. That type of backdrop favors the dollar over the euro, especially when the euro zone still lacks a convincing growth story.

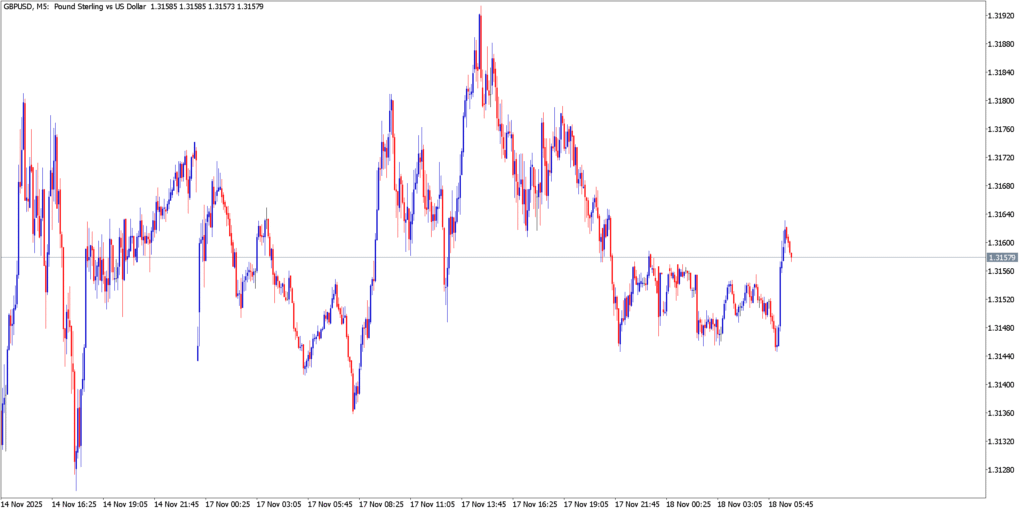

GBP/USD

Technical Analysis

GBP/USD ended the week on the defensive even if Friday’s move was more nuanced than Thursday’s sharp drop. Technically, the larger point was that the pair had failed to repair the damage of the earlier decline. Strong U.S. payrolls removed a potential reason to sell the dollar, while sterling never developed enough independent momentum to challenge that. So the pair finished the week looking more like a market consolidating losses than reversing them.

Fundamental Analysis

Sterling had already been hit hard by the war-and-oil story, and Friday’s payroll surprise did nothing to relieve that pressure. The pound still faced the same basic problem as earlier in the week: elevated energy costs complicated the UK inflation outlook, but did not automatically make sterling attractive. Against that backdrop, stronger U.S. hiring simply widened the contrast between a still-resilient U.S. macro picture and a more vulnerable UK one. That kept GBP/USD biased lower into the weekly close.

Market Outlook

The week ended with a familiar but now more refined hierarchy. The dollar remained broadly supported by war uncertainty, energy-linked inflation risk, and now a payrolls headline strong enough to reinforce Fed patience. Yet the details under that jobs report were softer than the top line suggested, which means the dollar’s support is solid but not invulnerable. The euro and pound remain weighed down by energy sensitivity, while USD/JPY remains the pair where macro support and policy danger are most directly colliding.