Tuesday closed the month and quarter with a complicated macro picture. Equities finished the quarter strongly, oil prices tumbled sharply, and the dollar held most of its June gains even as parts of the market began questioning how far the Fed-hike narrative could run. Reuters reported that stocks ended the quarter with big gains while oil posted one of its sharpest drops in years. The yen and gold also fell, underlining the continued dominance of higher U.S. yields and dollar carry in global markets.

The biggest FX story remained the yen. Reuters reported that Tokyo appeared to be keeping its “powder dry” as the yen broke through the long-defended 162-per-dollar level. Market participants increasingly viewed 165 as the next likely “line in the sand” for intervention, suggesting Japanese authorities were becoming more tolerant of yen weakness than during previous episodes.

This was a crucial shift in market psychology. In earlier months, traders treated 160–162 as a zone where official action could become imminent. By June 30, the market increasingly believed that Japan would avoid intervening unless the yen moved closer to 165 or volatility became disorderly. That allowed USD/JPY to stay elevated despite the obvious political discomfort.

Oil was the other major theme. The sharp decline in crude reduced inflation pressure globally, which should theoretically weaken the dollar by cooling Fed-hike expectations. However, lower oil also hurt commodity-linked currencies such as CAD, creating a mixed dollar picture across pairs.

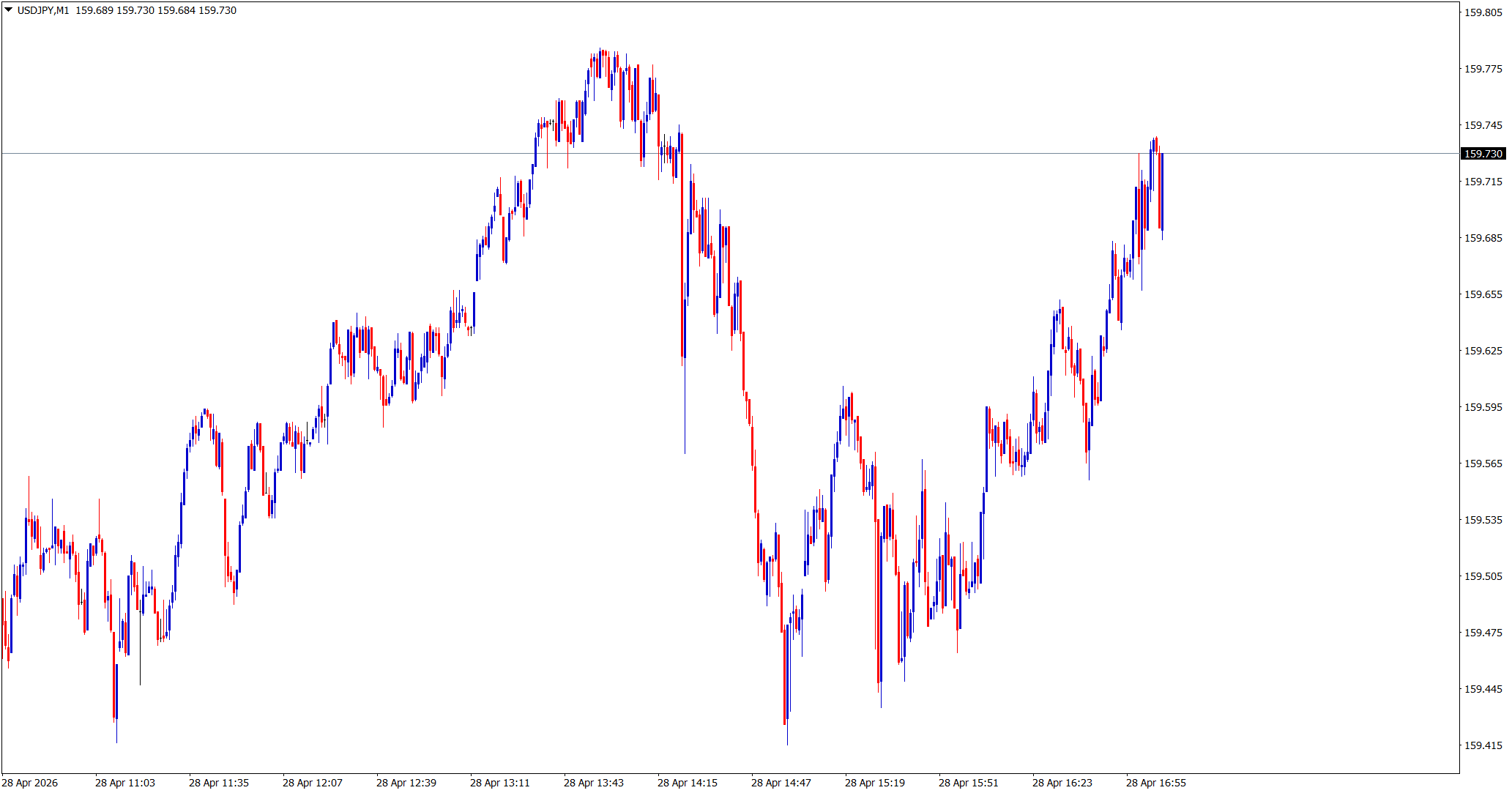

USD/JPY

Technical Analysis

USD/JPY remained elevated above the 162 area, holding near levels not seen since the 1980s. The pair’s technical structure remained bullish, with buyers continuing to defend dips and the broader trend still pointing higher.

What changed was the intervention psychology. The market no longer treated 162 as an automatic danger line. Instead, traders increasingly viewed the next critical zone as closer to 165. This allowed USD/JPY to maintain its upward structure with less immediate fear of official action.

Technically, the pair remained overextended, but not yet reversing. Momentum was still positive, and sellers lacked a clear catalyst. However, the higher the pair trades, the more vulnerable it becomes to sudden headline-driven pullbacks.

Fundamental Analysis

The fundamental driver remained yield divergence. Fed hike expectations and elevated Treasury yields continued supporting the dollar, while Japan’s policy framework remained comparatively loose. Even with the BOJ gradually normalizing, Japan’s absolute rate level remained far below the U.S.

Reuters’ analysis suggested Tokyo may prefer avoiding a fight at current levels because intervention would likely have only limited impact unless the underlying rate differential changes. That is critical. Intervention can slow a move, but if U.S. yields remain high and Japan’s fiscal backdrop stays loose, selling dollars may not permanently strengthen the yen.

Japan’s domestic policy picture also remained complicated. Fiscal expansion under Prime Minister Sanae Takaichi continued raising concerns about bond-market stability. That made aggressive BOJ tightening harder, even as yen weakness increased import costs. The result was a structural yen problem that intervention alone may not solve.

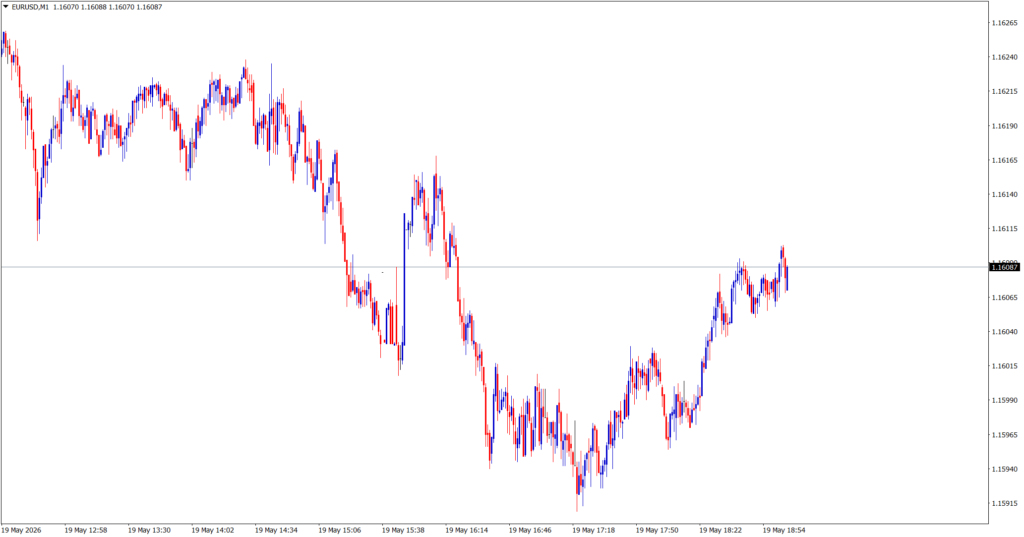

EUR/USD

Technical Analysis

EUR/USD stabilized after Monday’s rebound, but remained below the levels needed to confirm a deeper recovery. The pair traded with a calmer tone into quarter-end, suggesting that much of the immediate dollar-buying pressure had paused.

Technically, the euro was trying to build a short-term base after June’s sharp decline. However, the broader structure still favored sellers unless EUR/USD could reclaim broken support. The pair’s stabilization looked more like consolidation than a full reversal.

Quarter-end flows also likely contributed to choppy price action. After a strong monthly dollar performance, some rebalancing was natural, but that did not necessarily mean a new euro uptrend had begun.

Fundamental Analysis

The euro benefited modestly from falling oil prices, which reduce inflation pressure for energy-importing economies. Lower crude is generally supportive for Europe because it eases pressure on consumers and manufacturers.

However, the dollar still had the stronger policy story. Reuters’ broader June survey showed that the greenback remained supported by U.S. inflation above target, resilient economic growth, elevated Treasury yields, and signals that nearly half of Fed policymakers expected rates to rise this year.

That left EUR/USD caught between two forces: lower oil helping Europe, but Fed divergence helping the dollar. On Tuesday, those forces largely balanced out, keeping the pair in consolidation rather than driving a decisive move.

USD/CAD

Technical Analysis

USD/CAD traded firmer as oil weakness weighed on the Canadian dollar. The pair remained inside its broader range, but the short-term bias tilted upward as crude prices fell sharply into month-end.

Technically, the pair’s support held well. CAD buyers struggled to generate momentum because one of Canada’s biggest macro supports — oil — was weakening. Still, USD/CAD did not explode higher because the broader dollar rally was also losing some momentum after a strong June.

Fundamental Analysis

Falling oil created a clear headwind for CAD. Canada is a major energy exporter, so a sharp oil decline reduces terms-of-trade support for the currency. While lower oil can cool global inflation and eventually weaken the U.S. dollar, the first-order impact on CAD is often negative.

That made USD/CAD one of the clearer expressions of the oil move. The euro and yen can benefit from lower energy costs because Europe and Japan are importers. CAD, by contrast, loses a direct commodity tailwind. Reuters’ report that oil tumbled sharply into quarter-end helps explain why CAD underperformed relative to some other majors.

At the same time, USD/CAD’s upside was contained because traders were also questioning whether lower oil might reduce Fed hike pressure. The result was a firmer but still range-bound pair.

Market Outlook

June 30 ended a powerful month for the dollar, but also introduced reasons for caution. Oil’s sharp decline reduced inflation pressure, which could eventually cool Fed hike expectations. However, the dollar’s yield advantage remained intact, and USD/JPY continued to show that rate differentials still mattered more than official discomfort.

For now:

- USD/JPY remained bullish but increasingly politically sensitive.

- EUR/USD was stabilizing but not yet recovering decisively.

- USD/CAD was supported by falling oil and dollar yield strength.

- The market entered July watching whether lower crude would weaken the Fed-hike narrative or simply support risk assets without damaging the dollar.