Monday opened the final trading week of June with the dollar taking a modest step back, but without losing the broader strength it had built throughout the month. The greenback slipped slightly on the day, yet it remained close to 13-month highs and was still on track for its strongest monthly performance in nearly a year. The market’s core dollar-supportive themes remained intact: resilient U.S. growth, stubborn inflation risk, elevated Treasury yields, and the prospect that the Federal Reserve could still raise rates later in 2026. Reuters reported that the dollar index fell 0.28% to 101.08 but remained up 2.17% for June, while markets were still pricing a 64% chance of a Fed hike by September.

The session also carried a heavy geopolitical overlay. Weekend attacks by the U.S. and Iran reinforced the fragility of the interim peace deal, even though both sides later agreed to halt hostilities and resume talks. Oil prices rose more than 1% on Monday, with U.S. crude up 2.2% to $70.75 at one stage, as traders balanced renewed military risk against hopes that shipping through the Strait of Hormuz would continue recovering.

The yen was the standout weak currency. It touched a new 40-year low against the dollar, reflecting persistent pressure from wide U.S.-Japan yield differentials and doubts over how far Tokyo would go to defend the currency. Meanwhile, global equities held up well despite geopolitical tension, helped by easing fears that the latest U.S.-Iran flare-up would derail the fragile truce. Wall Street rose sharply, with the Dow hitting a record closing high as tech shares rebounded from the previous week’s selloff.

The result was a mixed but revealing FX session: the dollar eased versus the euro and pound after a strong monthly run, but USD/JPY remained structurally bid and commodity-linked pairs stayed sensitive to oil and geopolitical headlines.

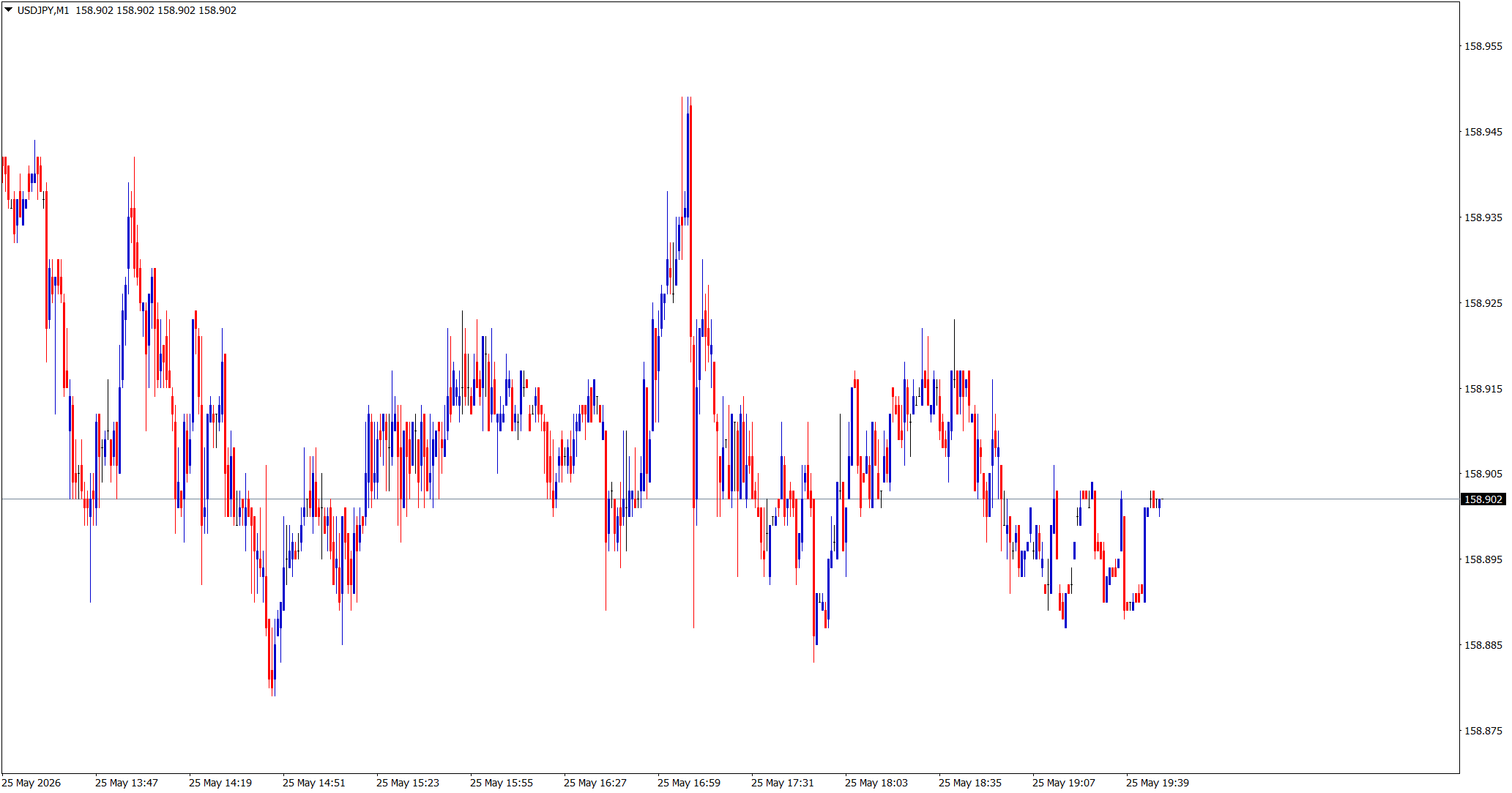

USD/JPY

Technical Analysis

USD/JPY remained the day’s most important pair as the yen weakened to its lowest level against the dollar in roughly four decades. The pair continued trading with an upward bias and remained firmly above the psychologically important 160 level, extending the broader bullish structure that had developed through June.

Technically, the move showed that the market was still willing to test Japanese policymakers. The pair’s strength was not just a short-term breakout; it was an extension of a longer trend defined by higher lows, persistent dip-buying, and strong yield-driven demand for dollars. However, price action near these levels is increasingly unstable. Once USD/JPY trades in territory associated with intervention risk, the market becomes less purely technical and more policy-sensitive.

The key technical issue is that the trend remains bullish, but the risk-reward becomes increasingly asymmetric. Momentum favors upside, but the threat of sudden verbal or actual intervention grows as the pair moves deeper into multi-decade highs. That means even if buyers remain in control, volatility risk is elevated.

Fundamental Analysis

The yen’s weakness was driven by the same structural forces that have dominated the pair for months: wide yield differentials, U.S. economic resilience, and Japan’s policy limitations. Markets continued pricing a meaningful chance of a Fed hike later in 2026, while the Bank of Japan remained far behind the Fed in absolute rate levels. That kept carry demand firmly tilted toward the dollar.

Japan’s energy dependence also remained a problem. Renewed U.S.-Iran strikes lifted oil prices, which is negative for Japan’s external balance because the country imports most of its energy. Higher oil increases import costs and inflation pressure without necessarily supporting domestic growth. That combination tends to weaken the yen, especially when U.S. yields remain high.

At the same time, intervention risk continued to build. The market was aware that Japanese officials were uncomfortable, but Monday’s price action suggested traders believed intervention would be difficult to sustain unless U.S. yields fell or the BOJ moved more decisively. Reuters noted that the yen touched a 40-year low, underlining just how deeply the pair had moved into policy-sensitive territory.

EUR/USD

Technical Analysis

EUR/USD recovered modestly as the dollar pulled back from its strongest levels of the month. The pair rose after recent weakness, but the move looked corrective rather than decisively bullish. The euro was rebounding from oversold short-term conditions after a difficult June, not yet establishing a strong upward trend.

Technically, EUR/USD remained below the levels it would need to reclaim to restore a constructive medium-term structure. The pair’s bounce improved the immediate tone, but it did not erase the damage caused by the June dollar rally. Former support areas continued acting as resistance, and the euro needed stronger follow-through to prove that Monday’s move was more than profit-taking in long-dollar positions.

The short-term picture therefore shifted from bearish continuation to stabilization. Buyers had some breathing room, but the broader trend still depended on whether Fed hike expectations softened further.

Fundamental Analysis

The euro benefited from the dollar’s slight pullback and from relief that U.S.-Iran tensions did not escalate into a larger energy shock. If oil prices remain contained, Europe gains because lower energy costs ease inflation pressure and support household purchasing power. That helped the euro stabilize.

However, the fundamental backdrop remained mixed. The dollar’s monthly strength was still supported by U.S. inflation above target, resilient growth, and elevated Treasury yields. Reuters noted that despite many strategists expecting eventual dollar weakness, the greenback had drawn support from strong U.S. growth, high yields, and June signals that nearly half of Fed policymakers expected rates to rise this year.

The eurozone’s own outlook remained less convincing. Growth was improving only gradually, and the ECB faced less pressure to sound aggressively hawkish than the Fed. That limited the euro’s upside even on a softer-dollar day. Monday’s EUR/USD rebound was therefore mainly a dollar-positioning move, not a full euro-led rally.

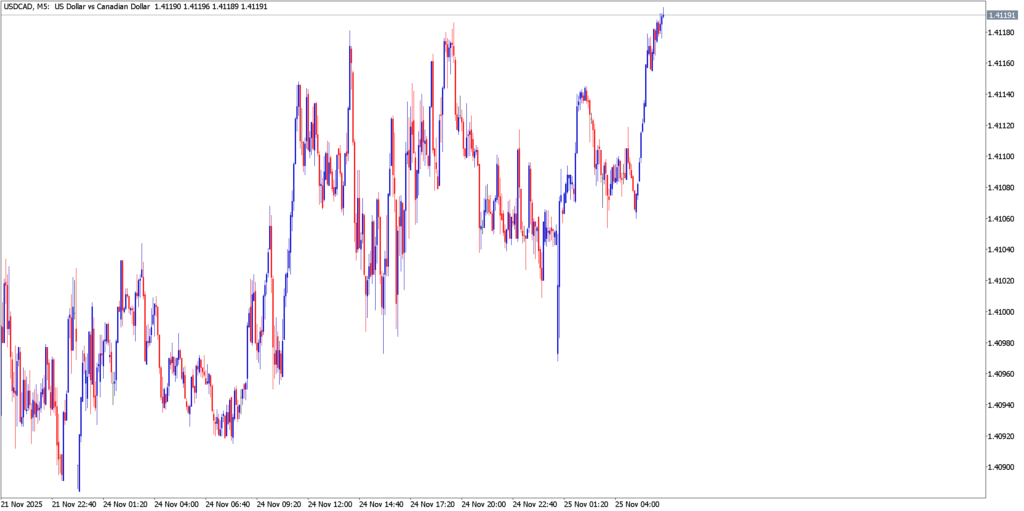

USD/CAD

Technical Analysis

USD/CAD traded with a firm underlying tone, reflecting the tug-of-war between a slightly softer U.S. dollar and firmer oil prices. The pair did not break aggressively higher, but it remained supported within its broader range. That suggested traders were not ready to sell dollars broadly, even though CAD had some help from crude.

Technically, USD/CAD remained range-bound rather than trend-driven. Recent support continued to hold, while upside momentum was limited by oil’s rebound. The pair’s behavior was consistent with a market balancing two opposing drivers: dollar yield strength and Canadian commodity support.

Fundamental Analysis

The Canadian dollar had a partial tailwind from higher oil prices after renewed U.S.-Iran strikes. Oil prices settled more than 1% higher as traders weighed the fragility of the interim peace deal against hopes that Strait of Hormuz shipping would continue normalizing.

Normally, firmer crude would support CAD more strongly. However, the broader dollar backdrop limited that effect. The dollar remained supported by Fed hike expectations and resilient U.S. data, while geopolitical risk also encouraged investors to maintain some defensive dollar exposure.

This made USD/CAD less clean than USD/JPY or EUR/USD. Higher oil helped Canada, but the dollar still retained enough macro support to prevent a decisive downside move. The pair remained a useful gauge of whether oil strength was being driven by healthy demand or by geopolitical risk. On Monday, the geopolitical element was strong enough to keep USD/CAD supported.

Market Outlook

June 29 showed that the dollar’s rally was stretched but not broken. Profit-taking allowed EUR/USD and GBP/USD to recover modestly, but the broader macro environment still favored the greenback as long as Fed hike expectations and Treasury yields stayed elevated.

The key themes heading into Tuesday were clear:

- USD/JPY remained the most politically sensitive major pair as the yen traded at 40-year lows.

- EUR/USD could recover if dollar longs continued taking profit, but euro fundamentals were not strong enough to lead alone.

- USD/CAD remained tied to whether oil’s rebound reflected lasting supply risk or temporary geopolitical noise.

- The dollar remained near major highs despite Monday’s dip, meaning the broader June uptrend was still intact.