Monday’s session opened the new week with a modest recovery in the U.S. dollar, but the move lacked the conviction that defined much of June’s dollar rally. After last week’s weak U.S. jobs report triggered the greenback’s largest weekly decline since April, traders used Monday to reassess whether the selloff had gone too far, or whether the Fed-hike narrative had genuinely weakened.

Reuters reported that the dollar index rose 0.24% to around 101.08, recovering slightly after last week’s payrolls-driven decline. The jobs report remained the dominant macro anchor: U.S. employers added only 57,000 jobs in June, much weaker than expected, which lowered market confidence in a near-term Federal Reserve rate hike. The euro hovered near two-week highs around $1.142, while sterling traded near $1.336 before slipping as its seven-day rally paused.

The broader global market backdrop was supportive but uneven. Wall Street rose as chip stocks continued rallying, with the Nasdaq gaining 0.92% and the S&P 500 up 0.42%, while investors looked ahead to major earnings from Delta Air Lines, PepsiCo, Samsung Electronics, and SK Hynix. Reuters also noted that oil prices stabilized near pre-conflict levels around $72.14 per barrel, helped by OPEC+ plans to raise output by 188,000 barrels per day from August and continued Strait of Hormuz ship traffic despite stalled U.S.-Iran peace talks.

That combination created a mixed FX environment. The dollar benefited from short-covering after last week’s slide and from persistent demand against the yen, but its upside remained capped by weaker labor data, lower Fed-hike odds, and calmer oil markets. Traders also shifted attention to this week’s FOMC minutes and ISM services data, which are expected to provide the next major clues on Fed Chair Kevin Warsh’s inflation stance and the durability of U.S. growth.

USD/JPY

Technical Analysis

USD/JPY remained the most important major pair on Monday because the yen stayed pinned near its weakest levels in roughly four decades. Reuters reported that the yen hovered around 162.3 per dollar, keeping the pair extremely close to intervention-sensitive territory. Technically, the pair remains in a high-level consolidation pattern rather than a clean reversal. The sharp pullback after last week’s weak payrolls report damaged upside momentum, but buyers have continued to defend dips, showing that the broader dollar-yen structure remains elevated and fragile rather than decisively bearish.

The 160–163 zone remains highly sensitive. Earlier in the year, traders treated 160 as a likely intervention danger area. By late June and early July, however, the market appeared to believe that Tokyo’s effective pain threshold may have shifted higher, closer to 165, unless volatility becomes disorderly. That is why USD/JPY has been able to remain elevated despite repeated official concern. Technically, this creates an unusual setup: the pair still has structural support from yield differentials, but every push higher carries rising headline and intervention risk.

Fundamental Analysis

Fundamentally, USD/JPY remains trapped between two powerful forces. On one side, last week’s weak U.S. jobs report reduced expectations for a near-term Fed hike and should, in theory, limit dollar upside. On the other side, Japan’s yield disadvantage remains severe. U.S. rates remain far above Japanese rates, and even after the payrolls miss, the dollar still offers a much more attractive carry profile than the yen.

Reuters noted that analysts are skeptical any Japanese intervention would provide lasting support unless the underlying interest-rate gap narrows. That matters because intervention can create sharp short-term yen rallies, but it rarely reverses a structural trend when yield differentials remain wide.

Japan also faces domestic pressure from yen weakness. A weaker yen raises import costs, especially for energy and food, and that has already become a political and economic issue. But tightening policy aggressively is difficult because Japan’s fiscal position and bond market remain fragile. That leaves USD/JPY supported by fundamentals even though the pair is politically uncomfortable at current levels.

GBP/USD

Technical Analysis

GBP/USD slipped on Monday, ending a seven-day rally that had been driven by last week’s dollar selloff and sterling’s strong performance against the euro. Reuters reported that the pound fell about 0.1% to $1.3338, after gaining 1.1% last week, its strongest weekly advance in roughly three months.

Technically, the pullback looked corrective rather than trend-changing. Sterling had become stretched after a strong run, and Monday’s decline reflected profit-taking as the dollar steadied. The pair remained near the upper end of its recent range, meaning the broader recovery structure was not broken. However, the failure to extend higher after the seven-day rally suggests that GBP/USD now needs fresh catalysts to continue advancing.

The key technical point is that sterling is still constructive, but no longer accelerating. If buyers defend the $1.33 area, the pair can remain supported. A deeper break below recent support would suggest the rally has exhausted itself.

Fundamental Analysis

Sterling’s Monday weakness reflected both broad dollar stabilization and UK-specific uncertainty. Reuters noted that falling oil prices near $70 per barrel have eased inflation pressure and reduced the probability of aggressive central-bank rate hikes, including from the Bank of England. Markets currently price only about a 70% chance of one BoE hike this year, while Governor Andrew Bailey has reiterated that rate cuts are not being considered.

That creates a complicated environment for the pound. Lower oil helps the UK economy because Britain is exposed to imported energy costs, but it also reduces the urgency for BoE tightening. Meanwhile, a BoE survey showed UK businesses expect prices to rise 4.1% over the next year, suggesting inflation psychology remains sticky despite easing energy prices.

Politics also remains a drag. Reuters reported continued uncertainty over who could become Chancellor if Andy Burnham succeeds Keir Starmer around July 20, with speculation around Ed Miliband raising concerns over potentially more fiscally expansive policies and the impact on UK bond yields.

So GBP/USD is supported by reduced Fed-hike expectations and sterling’s recent strength, but capped by UK political uncertainty and a less clearly hawkish BoE outlook.

EUR/USD

Technical Analysis

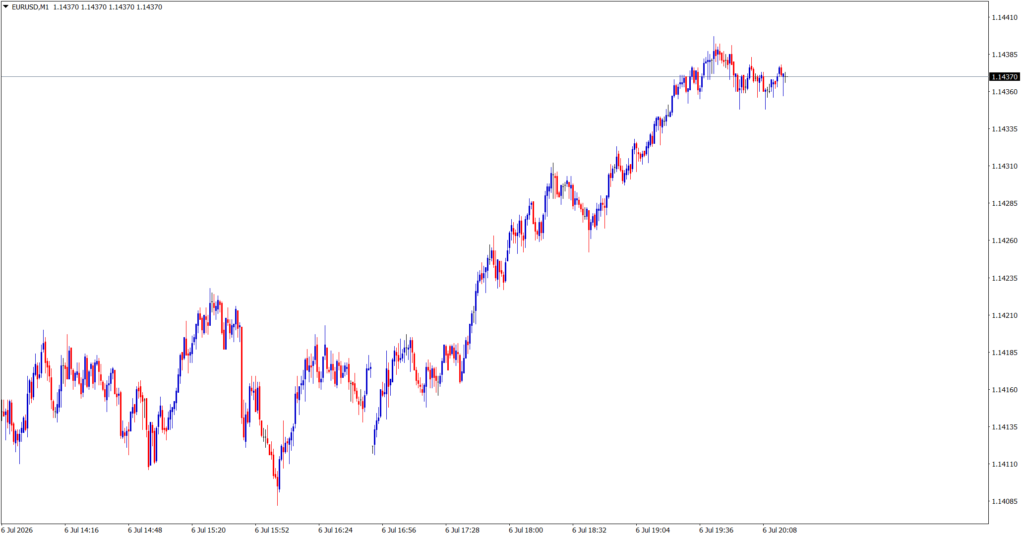

EUR/USD held near two-week highs around $1.142, showing that the euro retained most of last week’s recovery even as the dollar edged higher on Monday. The pair did not extend its rally, but it also avoided a sharp pullback, suggesting that sellers remain cautious after the weak U.S. payrolls report weakened the Fed-hike narrative.

Technically, EUR/USD is trying to turn last week’s rebound into a base. The pair has recovered from the late-June selloff, but it still needs a stronger break above recent resistance to confirm a broader bullish reversal. Monday’s session looked like consolidation after a strong recovery rather than renewed euro weakness.

The short-term structure is therefore balanced. Buyers have regained control compared with late June, but the pair still lacks enough momentum to force a major breakout without another dollar-negative catalyst.

Fundamental Analysis

The euro’s support came mainly from the dollar side. The weaker U.S. jobs report lowered Fed-hike expectations and reduced the dollar’s yield advantage, allowing EUR/USD to stabilize near recent highs. However, the euro’s own fundamental backdrop remains mixed.

Reuters reported that the European Stability Mechanism warned the euro zone could face recession if a renewed Middle East conflict and a major U.S. asset selloff hit simultaneously. The ESM said euro-area exposure to U.S. financial markets has risen to 47% of GDP in 2025, up from 18% in 2013, making Europe more vulnerable to a U.S. market shock. It also warned that a combined U.S. asset repricing and renewed Middle East conflict could push eurozone inflation close to 5% and cause contraction in 2027.

That warning is important for EUR/USD because it highlights Europe’s vulnerability to external shocks. The euro can rally when the dollar weakens, but the region remains exposed to global equity repricing, U.S. financial-market volatility, Middle East energy shocks, and private credit risks. Those vulnerabilities limit the euro’s ability to lead a sustained rally unless the U.S. dollar story weakens more decisively.

At the same time, stable oil near pre-conflict levels helps Europe by reducing imported inflation pressure. That provides a modest cushion for the euro, especially compared with June’s oil-driven inflation scare. But for now, EUR/USD remains more of a dollar-weakness trade than a euro-strength trade.

Market Outlook

July 6 was a reset session rather than a trend day. The dollar recovered slightly after last week’s large decline, but the rebound did not invalidate the payrolls-driven shift in market expectations. The U.S. jobs report remains the key turning point: a weak 57,000 payroll print made traders less confident that the Fed can hike soon, even though U.S. yields and AI-driven capital flows still give the dollar underlying support.

The week ahead will be important because investors are moving from payrolls to policy and profits. The FOMC minutes and ISM services data will test whether the Fed’s hawkish June tone still holds after weaker labor-market data. Meanwhile, U.S. corporate earnings, especially in technology and semiconductors, will influence whether AI-driven equity flows continue supporting U.S. assets and, indirectly, the dollar.

For now:

- USD/JPY remains elevated and intervention-sensitive, with the yen near 40-year lows.

- GBP/USD has paused after a seven-day rally, weighed by profit-taking and UK political uncertainty.

- EUR/USD is holding near two-week highs but remains dependent on continued dollar softness.

- The dollar is no longer in the strong, one-way Fed-hike rally seen in late June, but it has not lost its broader yield and capital-flow support either.

The market’s next major move will likely depend on whether upcoming U.S. data and Fed minutes confirm the post-payrolls cooling narrative, or restore confidence that another Fed hike remains firmly on the table.