Wednesday began July with the dollar still supported, but the session became more nuanced after Federal Reserve Chair Kevin Warsh indicated that inflation expectations and inflation risks had eased in recent weeks. Reuters reported that the dollar gained ahead of the closely watched U.S. jobs report but pared earlier increases following Warsh’s comments. Fed funds futures still priced a 66% chance of a September hike, but the Chair’s remarks softened the market’s conviction that inflation pressure was still building.

The euro came under pressure after data showed eurozone inflation fell more than expected in June to below 3%, reducing some of the pressure on the European Central Bank to raise rates. Reuters reported that the euro fell 0.39% to $1.1376, while the dollar index rose 0.17% to 101.41.

At the global level, markets were still absorbing the impact of June’s major moves: a strong dollar, a weak yen, falling oil, and stretched equity valuations. Stocks were mixed, oil fell, and traders prepared for a U.S. jobs report that could either revive Fed-hike expectations or confirm that the labor market was cooling.

This created a cautious session: the dollar retained support, but Warsh’s comments prevented a more aggressive breakout.

EUR/USD

Technical Analysis

EUR/USD weakened and remained under pressure after eurozone inflation data. The pair traded near recent lows and failed to generate meaningful upside, confirming that the euro’s recovery attempt from late June remained fragile.

Technically, EUR/USD was still in a bearish short-term structure. The pair’s inability to reclaim the $1.14 area after repeated attempts showed that sellers remained active. The decline toward $1.1376 reinforced the idea that broken support had become resistance.

Momentum remained weak, though not yet disorderly. The pair needed either softer U.S. data or a meaningful shift in Fed pricing to stabilize more convincingly.

Fundamental Analysis

The euro was hit by softer inflation data. Eurozone inflation falling below 3% reduced pressure on the ECB to tighten further, especially given the region’s weak growth profile. That widened the policy contrast with the U.S., where markets were still pricing a meaningful chance of a Fed hike.

The U.S. side was more complicated. Warsh’s comments that inflation risks had eased softened the dollar late in the session, but they did not fully erase Fed-hike expectations. The market still saw the U.S. economy as stronger and more inflation-prone than the eurozone.

This left EUR/USD under pressure. The euro had little independent support, while the dollar retained a yield advantage even after paring gains.

USD/JPY

Technical Analysis

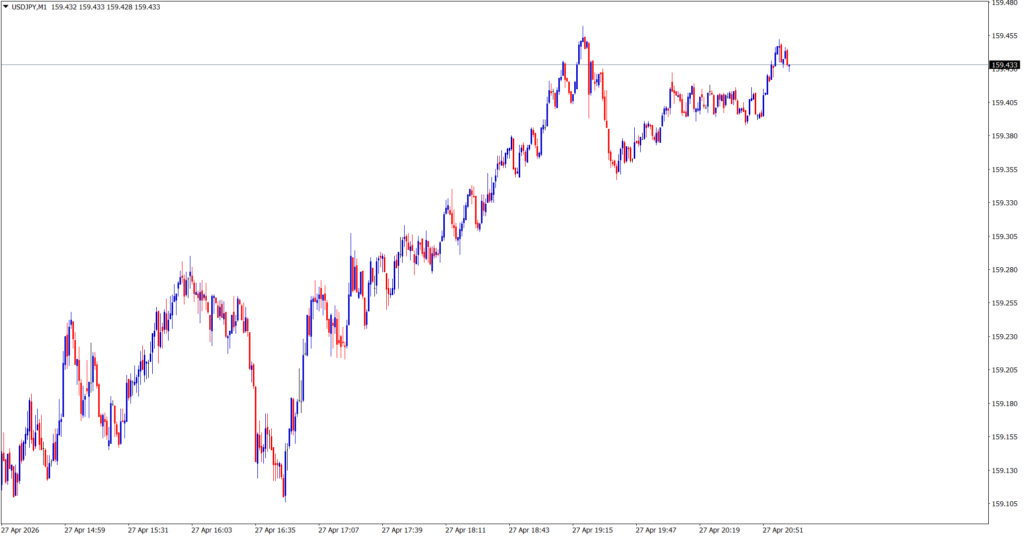

USD/JPY remained near extreme levels, with the yen little changed around 162.56 per dollar. The pair held its elevated range despite Warsh’s softer inflation comments, showing that dollar-yen remained structurally supported.

Technically, USD/JPY remained bullish but stretched. The pair had already broken above the long-defended 162 level, and traders were increasingly watching the 165 area as the next possible official pain threshold. The lack of a sharp reversal suggested that intervention fears were not enough to trigger sustained yen buying.

Fundamental Analysis

The dollar-yen story remained dominated by U.S.-Japan rate differentials. Even after Warsh said inflation risks had eased, markets still priced a September Fed hike as more likely than not. That kept U.S. yields attractive relative to Japan.

The yen also suffered from doubts over the effectiveness of intervention. Reuters reported the previous day that Tokyo appeared to be shifting its “line in the sand” toward 165, making traders less cautious around 162.

Japan’s fiscal backdrop also remained a concern. Expansionary fiscal policy and rising JGB yields complicated the BOJ’s ability to tighten aggressively. That meant the yen lacked a strong domestic anchor, leaving USD/JPY elevated even when the broader dollar pared gains.

GBP/USD

Technical Analysis

GBP/USD held up better than EUR/USD, reflecting sterling’s relative strength in European FX. While the pair faced dollar pressure, it did not break down as decisively as the euro. This showed that sterling was receiving support from cross-flow dynamics, particularly its strength against the euro.

Technically, GBP/USD remained range-bound but resilient. The pair needed a weaker dollar to rally decisively, but its downside was cushioned by relative GBP strength.

Fundamental Analysis

Sterling’s resilience was linked to euro weakness and UK-specific positioning. Reuters technical commentary noted that the euro had repeatedly failed to clear key levels against the pound, with EUR/GBP locked in a losing battle. That helped sterling hold up even as the dollar remained firm.

The UK backdrop was not without risks. Political uncertainty around Andy Burnham’s expected leadership transition and fiscal policy remained a concern, but markets were also pricing the Bank of England as less likely to cut rates. That gave sterling some support against the euro, even if it struggled to outperform the dollar.

GBP/USD therefore traded as a relative story: weaker than it would be in a soft-dollar environment, but stronger than EUR/USD because sterling had its own cross-market support.

Market Outlook

July 1 left markets focused squarely on the U.S. jobs report. The dollar was still supported by Fed-hike expectations, but Warsh’s comments introduced the possibility that inflation pressure may be easing. That made payrolls even more important.

For now:

- EUR/USD remained under pressure after softer eurozone inflation.

- USD/JPY stayed elevated as intervention risk failed to offset yield differentials.

- GBP/USD was cushioned by sterling’s relative strength against the euro.

- The dollar’s next major move depended on whether jobs data confirmed or challenged the Fed-hike narrative.