Wednesday was the day the market effectively decided Tuesday’s relief move had gone too far. Reuters reported that the dollar rose as investors remained on edge about the Middle East war, with Iran’s military command warning the world should prepare for oil at $200 a barrel and further ships coming under attack in the Gulf. At the same time, Reuters’ market wrap said oil prices settled up nearly 5%, global stocks fell, and Treasury yields climbed. That combination, higher oil and higher yields together, is exactly the sort of macro mix that tends to rebuild the dollar bid fast.

This was also the session in which inflation fear became even more central than safe-haven demand. Reuters noted the dollar had risen about 2% against the euro since the end of February on a flight to safety, but by Wednesday the story was clearly broader than shelter. Rising oil and rising yields meant the market was increasingly treating the conflict as an inflationary event that could delay easing by multiple central banks. That is a more durable foundation for dollar strength than pure fear alone.

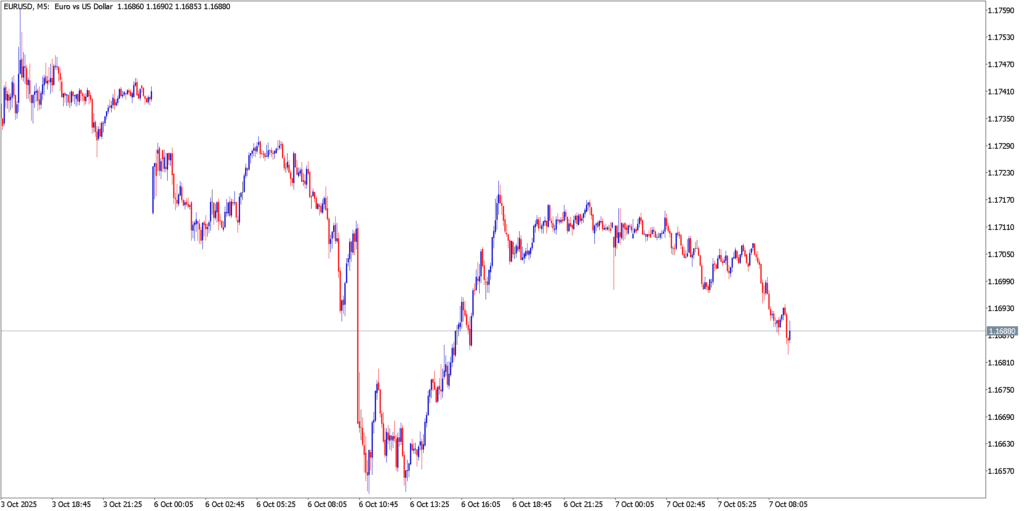

EUR/USD

Technical Analysis

EUR/USD resumed weakening, and the way it weakened mattered. Reuters reported the euro fell around 0.34% to about $1.157. That is not a violent one-day collapse, but it is the kind of persistent slide that confirms the market is re-establishing a bearish trend after a temporary interruption. Technically, Wednesday looked like a failed rebound day confirmed by renewed selling, which is usually more meaningful than a simple continuation lower.

Fundamental Analysis

The euro’s problem remained the same, but Wednesday sharpened it. Oil was pushing higher again, yields were rising, and ECB President Christine Lagarde was stressing the need to keep inflation under control and avoid a repeat of the 2022 energy shock. Those are not comforting conditions for the single currency. Europe still looked like one of the regions most directly exposed to imported energy inflation, while the U.S. dollar benefited from safety demand and higher relative yields. EUR/USD therefore became a very clean trade again: short euro, long dollar, under an inflation-risk regime.

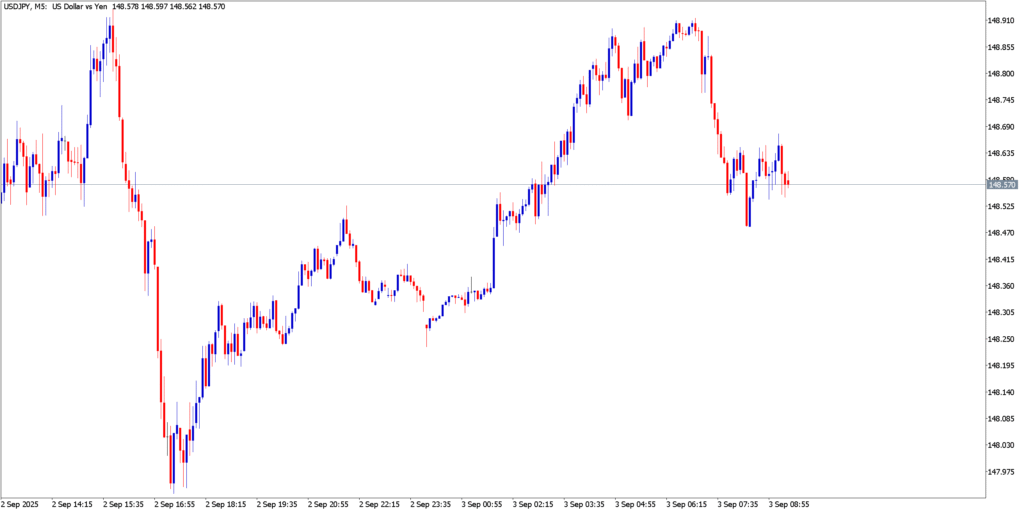

USD/JPY

Technical Analysis

USD/JPY pushed higher and Reuters reported the dollar was up about 0.6% at 158.9. That is important because Wednesday’s environment, higher yields and renewed dollar confidence, gave the pair a much cleaner directional logic than it had earlier in the week. Technically, the move looked like the pair was reasserting its broader uptrend rather than merely bouncing around headlines. The fact that it could approach the upper end of recent ranges even while the yen retained haven characteristics showed how powerful the yield side of the equation had become.

Fundamental Analysis

The yen had a hard time competing against this backdrop. Japan was still vulnerable to higher imported energy costs, and once U.S. yields rose again, the yen’s haven advantage was no longer enough to offset the widening policy and rate gap. Reuters’ commentary on the day made clear that markets were back to worrying about prolonged conflict and higher oil, and in that environment the U.S. dollar remained the preferred haven. That pushed USD/JPY higher even though, in a pure geopolitical scare, one might normally expect more yen support.

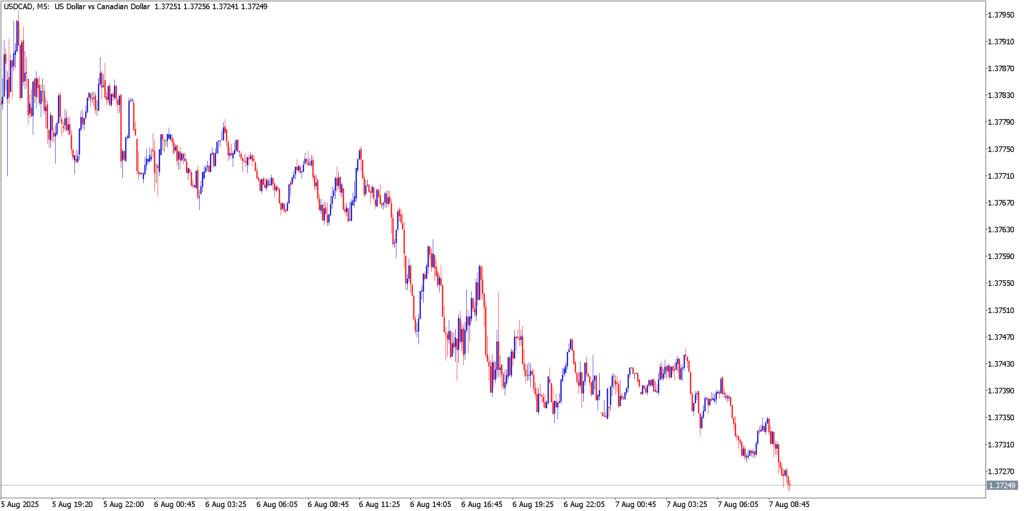

USD/CAD

Technical Analysis

USD/CAD stayed firmer than one would normally expect with oil so strong, and Reuters specifically reported that the Canadian dollar edged lower as higher oil prices failed to spur the currency. That is a significant technical and macro tell. When a currency refuses to rally on what should be one of its clearest bullish inputs, it usually means the countervailing force is strong. In this case, that force was renewed broad-based dollar demand.

Fundamental Analysis

Reuters’ Canadian coverage showed just how dominant the U.S. dollar story was on Wednesday. Yes, oil was surging, which should support Canada. But Reuters also noted that Canada’s oil producers said little could be done to boost production in the short term, which limited how much the market could extrapolate oil strength into improved macro support for CAD. At the same time, rising U.S. yields and a stronger dollar made it difficult for the loonie to outperform. So USD/CAD held up not because oil stopped mattering, but because the dollar side of the pair mattered more.

Market Outlook

By Wednesday’s close, the market had largely re-embraced the stronger-dollar regime. Tuesday’s optimism had not been disproven in theory, but it had been overtaken in practice by higher oil, higher yields, and more conflict stress. That restored EUR/USD and USD/JPY as core macro trades and showed that even commodity currencies like CAD could struggle if the U.S. inflation-yield story regained dominance.

Discover our other forex market analyses: